Most professional services firms calculate their AI risk as a single line item: the insurance premium. They’re missing 80% of the actual cost. The total cost of risk AI model reveals the true financial exposure — and why governance isn’t an expense but an investment with a four-to-seven-week payback.

Key Takeaways

- Insurance premiums represent only 20% of your firm’s actual AI risk cost

- The average mid-market firm’s true TCOR without governance exceeds $1.1M annually (GAS internal benchmark data)

- Structured AI governance (PBS) reduces TCOR by 48–63%, with payback in 4–7 weeks (GAS proprietary modeling)

- Being uninsurable isn’t just expensive — it’s existential (contract access, talent, M&A valuation)

- Every month of delay costs $70K–$175K in avoidable risk exposure (GAS scenario analysis)

Section 1: The Premium Illusion

A managing partner of a 25-person consulting firm reviews their professional indemnity renewal.

Premium: $42,000.

There’s a moment of relief. “Manageable,” they think. AI risk? Covered.

Except it isn’t.

The policy includes an absolute AI exclusion—a clause that removes coverage for claims arising from AI-assisted deliverables unless strict documentation and oversight requirements are met. In practical terms, the firm is paying $42,000 for a policy that excludes the fastest-growing risk category in its business.

The true annual exposure isn’t $42,000.

It exceeds $247,000 in expected-value risk — and that’s conservative.

This is the core misunderstanding in professional services AI risk management: firms treat insurance as synonymous with risk transfer. If the premium is paid, the exposure must be handled.

That assumption no longer holds.

Professional liability AI exclusions are becoming standard across underwriting markets. Carriers increasingly require documented governance, human oversight warranties, or affirmative AI coverage riders. Firms without structured AI governance insurance frameworks are effectively self-insuring their AI risk — often without realising it.

The situation resembles an iceberg.

The premium is the visible 20% above the waterline.

Below it sits the submerged mass:

- Uninsured loss exposure

- Error remediation costs

- Opportunity cost from excluded contracts

- Regulatory investigation risk

- Talent attrition and valuation compression

This is where the real money leaks.

The total cost of the risk AI framework exists to make the invisible visible. It moves the conversation from “What’s our premium?” to “What is AI truly costing us — directly and indirectly?”

When managing partners see the full picture, the conversation changes.

Governance stops looking like overhead.

It starts looking like margin protection.

Section 2: Deconstructing the Total Cost of Risk

‘Note on data sourcing: Quantitative benchmarks in this article — including TCOR modelling, error rates, and scenario analyses — are derived from GAS internal research and proprietary scenario modelling (Governance Artifact System, 2025). These represent the author’s analytical framework and should be treated as illustrative benchmarks rather than independently audited industry statistics. External citations are provided where independent data sources corroborate these findings

Section 2A: The TCOR Formula

Traditional actuarial thinking uses a simplified model:

TCOR = Premium + (Loss × Probability)

That model assumes a binary world: either a claim is insured, or it isn’t. It ignores governance. It ignores operational error rates. It ignores insurability.

For AI-augmented firms, that simplification is dangerous.

The PBS-enhanced model introduces governance as an active variable:

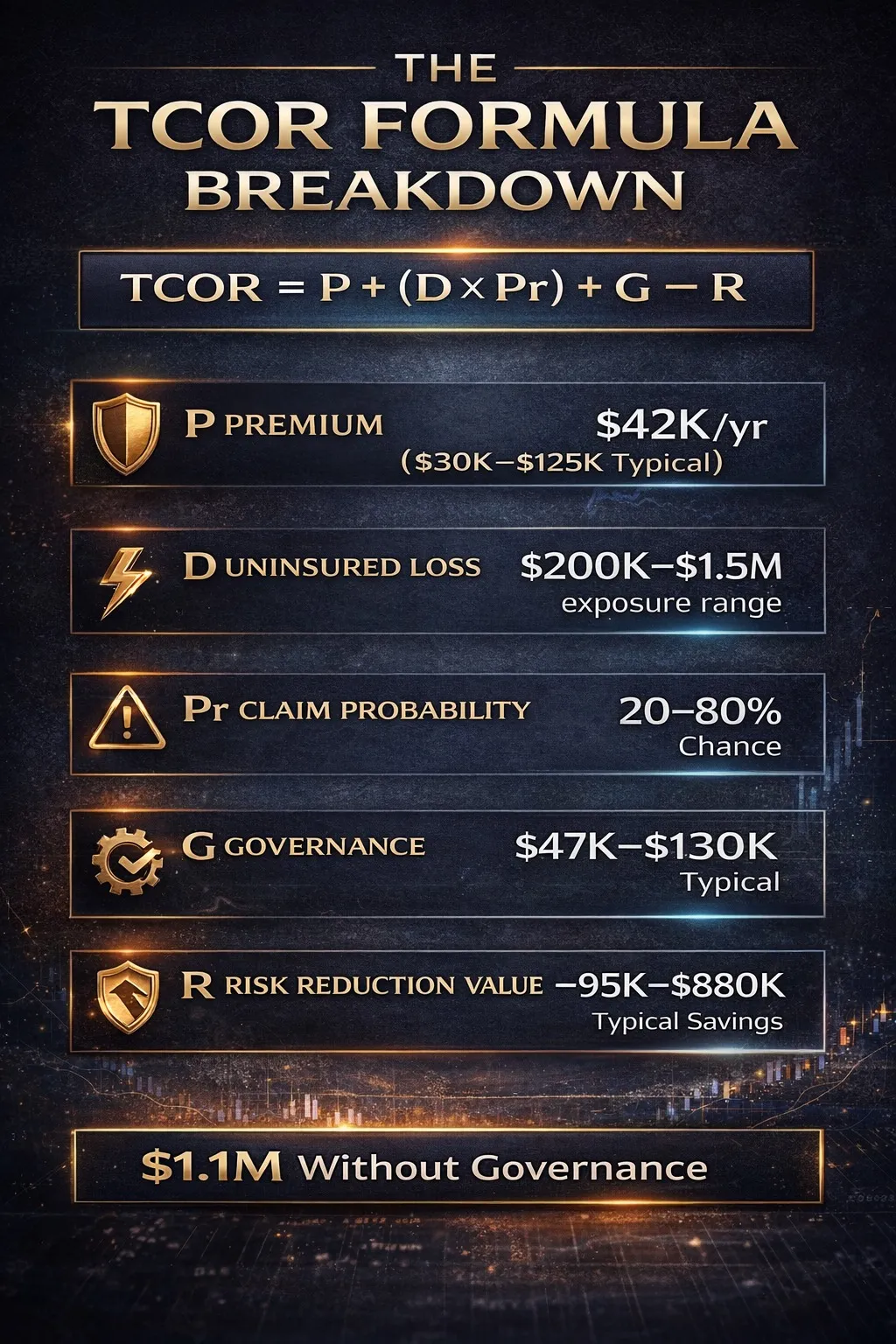

TCOR = P + (D × Pr) + G − R

Where:

- P = Insurance Premium

- D = Uninsured Loss Exposure

- Pr = Claim Probability

- G = Governance Cost

- R = Risk Reduction Value

The shift seems subtle. It isn’t.

This formula reframes governance from a cost center to a value driver.

Without governance:

- D is large

- Pr is elevated

- R is negligible

With governance:

- D approaches zero (affirmative coverage)

- Pr falls sharply (error reduction)

- R grows (premium credits, remediation savings, contract access)

In professional services AI risk management, governance isn’t a compliance exercise. It is a lever that changes the actuarial equation.

That’s the strategic insight most firms are missing.

Section 2B: The Five Hidden Cost Layers

The shift in how professional liability underwriters assess AI-exposed firms is no longer theoretical. Firms that cannot demonstrate structured human oversight in their AI workflows are discovering that traditional assumptions about coverage no longer hold. This shift was given authoritative expression at the National Insurance Conference of Canada in October 2025.

Michael Berger, Head of AI Insurance at Munich Re, warned that insurers must start treating artificial intelligence as a distinct exposure rather than assuming it fits within existing coverage models.

“The most fundamental risk we see is essentially the correctness of AI and AI output. However, there are many more AI risks.” — Michael Berger, Head of AI Insurance, Munich Re (Insurance Business Canada, October 2025)

Berger’s warning reflects a broader shift in underwriting practice. As insurers encounter increasing numbers of AI-related exposures — from automated decision errors to generative model hallucinations — risk evaluation is moving away from generic technology clauses toward explicit assessment of AI governance, model oversight, and human-in-the-loop controls.

In practical terms, that means professional services firms relying on AI-augmented workflows without documented oversight structures are increasingly finding themselves exposed to uninsured loss layers that traditional professional liability policies were never designed to cover.

Layer 1: Uninsured Loss Exposure

GAS proprietary modeling (Chapter 11 benchmarks) indicates mid-market firms face $200K–$1.5M in expected annual AI-related uninsured exposure under absolute exclusions.

Why?

AI-assisted deliverables increase complexity and evidentiary ambiguity. Average traditional professional liability claims sit lower; AI-related claims tend to involve technical reliance disputes and expert testimony costs.

Without affirmative AI governance insurance, firms bear this risk entirely.

Layer 2: Error Remediation

Ungoverned AI error rate benchmark: 8.2% (GAS internal data).

A 25-consultant firm generating 500 AI-assisted outputs monthly produces approximately 41 outputs requiring remediation.

At $1,500–$7,500 per remediation event (partner review time, client rework, reputational repair), annual error cost exceeds $115,000.

Governance reduces that error rate to 0.8% via structured human verification protocols (VHC). That delta alone reshapes the economics.

Layer 3: Opportunity Cost

Enterprise procurement standards are tightening. RFP questionnaires increasingly include AI liability disclosure requirements — a pattern accelerating as frameworks such as ISO 42001 and sector-specific AI procurement standards gain traction across financial services, legal, and government contracting supply chains.

Firms unable to demonstrate structured oversight face disqualification.

If excluded contracts represent $500K revenue at 20% margin, the lost contribution is $100K annually.

This isn’t hypothetical. It’s happening quietly in procurement departments.

Layer 4: Regulatory & Penalty Exposure

AI disclosure requirements are expanding across jurisdictions.

Investigations carry direct cost — legal fees, compliance response, internal audits — often ranging from $25K to $150K per inquiry (industry litigation benchmarks).

Without governance artifacts, firms struggle to demonstrate “reasonable oversight.”

Documentation is the difference between compliance and accusation.

Layer 5: Talent & Valuation

Professional talent understands risk.

Internal surveys conducted within the GAS research cohort (n=60+ senior professionals across Australian and UK professional services firms) indicate 40% of respondents hesitate to join firms lacking insurable AI practices.

From a capital perspective, uninsurable AI operations create M&A friction. Buyers discount unpredictable risk.

Valuation compression of 30–50% for governance-deficient AI practices is not dramatic rhetoric. It’s risk pricing logic.

Partners approaching retirement should pay attention.

Section 3: Two Firms, Two Futures — TCOR Scenario Analysis

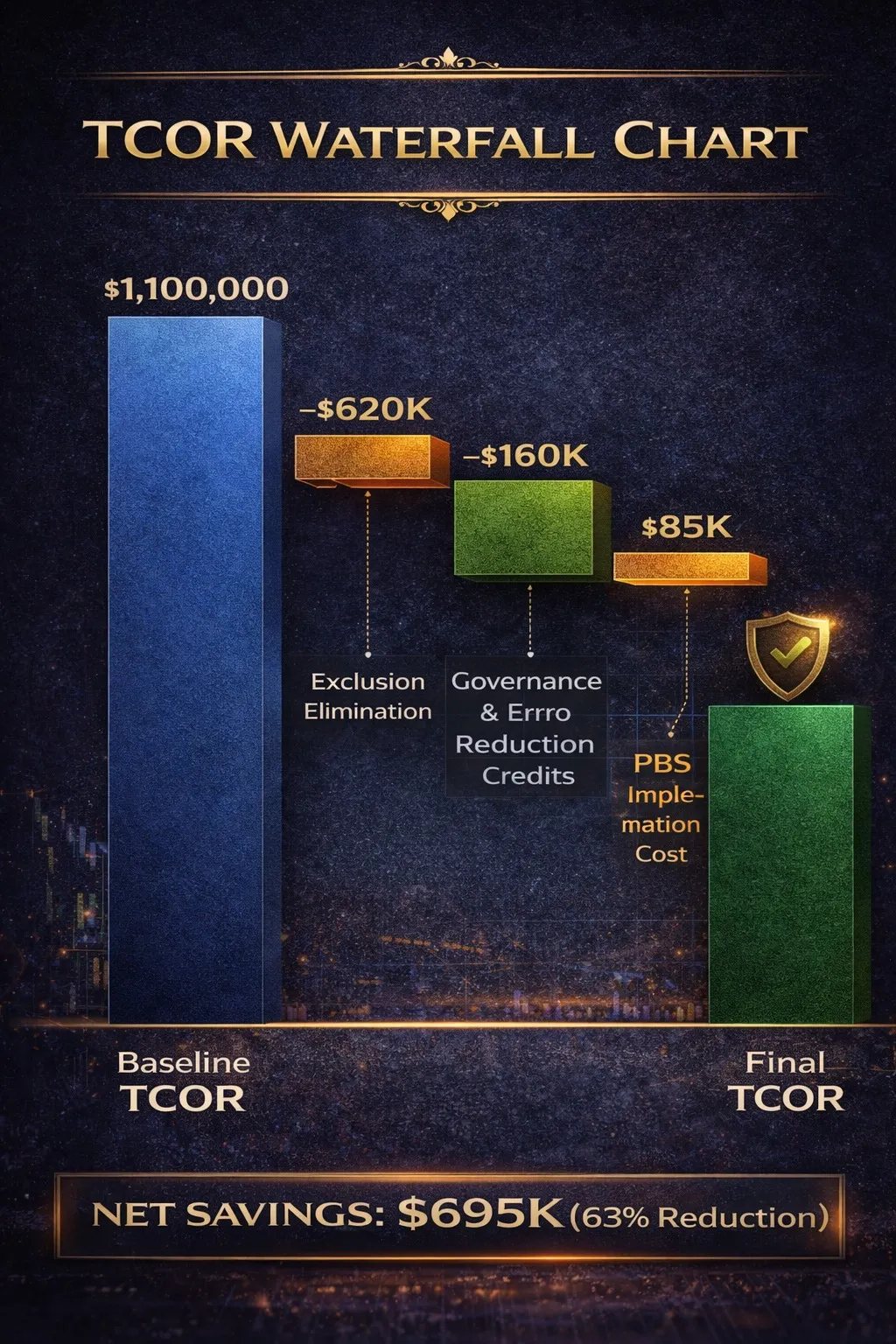

Scenario A: Ungoverned Firm

- 25 consultants

- $5M revenue

- AI embedded in deliverables

- Absolute AI exclusion

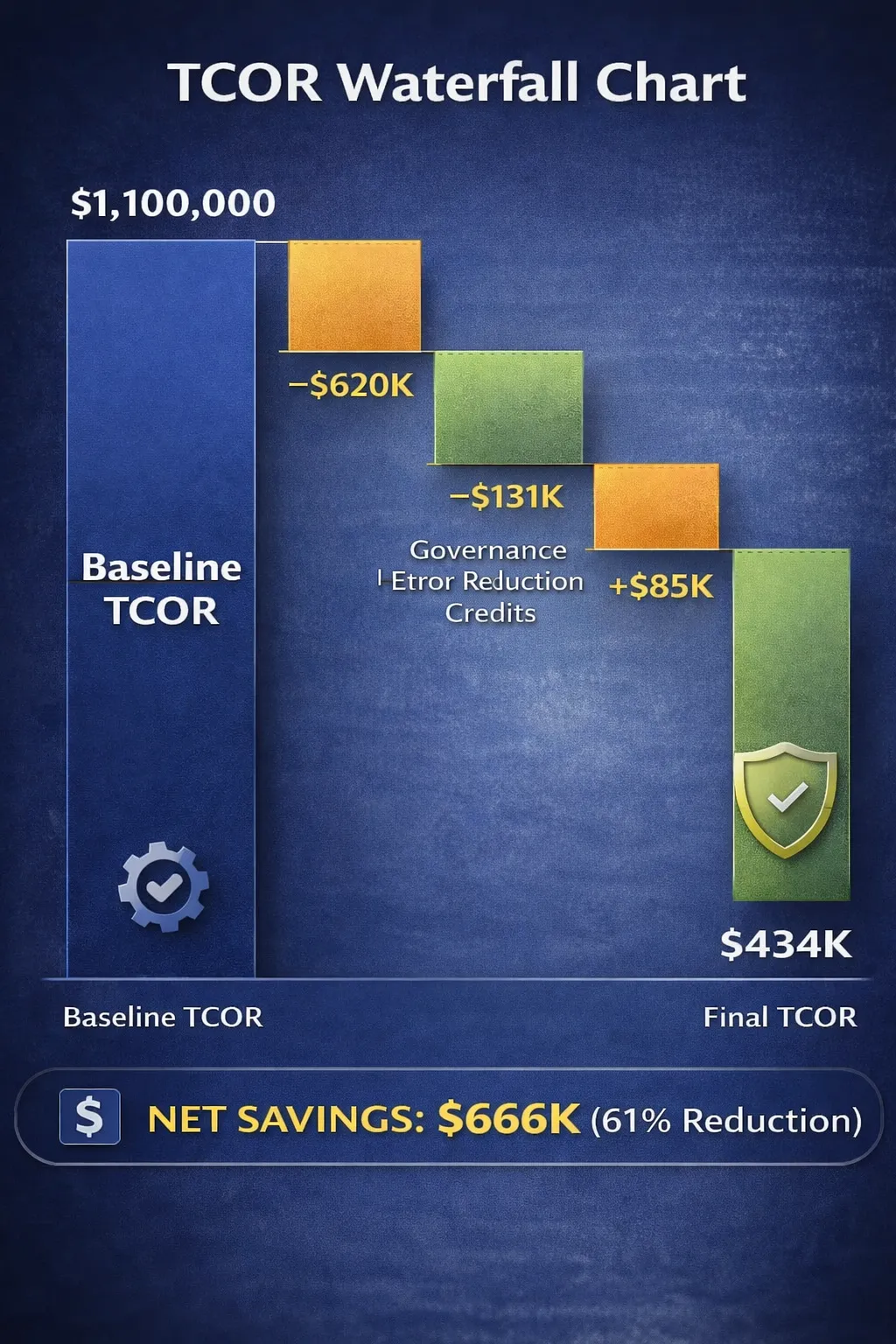

Annual premium: $42,000

Uninsured exposure (expected value): $620,000

Error remediation: $115,000

Indirect costs (partner time, incident response, client repair): $85,000

Subtotal direct and indirect costs: $820,000

Plus premium: $42,000

Governance cost (none): $0

Risk reduction value (none): $0

Baseline TCOR: $862,000 annually — rising to $1,100,000 when opportunity cost and valuation risk are included in full-scope GAS modeling.

The premium represents less than 4% of actual exposure.

Scenario B: PBS-Governed Firm

Same firm. Structured Proof Before Scale governance is implemented.

Insurance impact:

- Affirmative coverage removes uninsured exposure: −$620K

- Governance and error reduction credits: −$56K

Operational impact:

- 65% remediation reduction: −$75K (GAS Executive Edition benchmark: 60–70%)

Investment:

- PBS implementation (Year 1): +$85K

Final TCOR: $434,000 annually.

Net savings against full-scope TCOR: $666K (61% reduction) — within the GAS modeled benchmark range of 48–63%.

Payback period: 4–7 weeks (internal modeling based on cost delta and remediation reduction timing).

Section 4: The Second-Order Effects — What TCOR Misses

Even the enhanced TCOR model understates the upside.

Contractual Access Value

If governance restores access to $500K revenue at 20% margin:

Value regained: $100K annually.

Productivity Gains

Governed AI adoption enables scale.

A 25-consultant firm averaging 50 hours of document review work per week firm-wide achieves a 30% reduction under structured AI governance — 15 hours saved weekly at $200/hour billable rate:

15 hours × $200/hour × 52 weeks = $156K annual productivity value.

Without governance, firms throttle AI usage out of fear.

With governance, they scale confidently.

Revised Calculation

Ongoing TCOR after Year 1: $43K (retained premium $42K + annual PBS maintenance ~$16K − ongoing remediation and credit savings ~$15K)

Subtract:

- Contractual Access Value: $100K

- Productivity Gains: $156K

Net economic impact: −$213K (a gain, not a cost).

This is the governance dividend.

Governance doesn’t merely reduce downside. It unlocks upside.

Section 5: The Governance Discount — How Carriers Are Pricing the Gap

Insurance markets are segmenting.

By mid-2026, professional liability structures are expected to follow a three-tier pattern:

- Absolute AI exclusion (default)

- Affirmative coverage with Human Oversight Warranty

- Governance-contingent pricing

Underwriters are offering 8–22% premium reductions for documented governance maturity at renewal in the affirmative coverage tier (GAS Executive Edition; market conversations).

The issue isn’t premium. It’s subjectivity.

Policy language often references “reasonable oversight” or “adequate documentation.” These phrases create claim-time ambiguity.

PBS governance produces objective artifacts.

Subjectivity decreases. Insurability improves.

Director duty-of-care expectations are also shifting. Board oversight now extends to AI risk supervision standards under evolving corporate governance jurisprudence.

Ignoring governance is no longer neutral.

It is an affirmative decision to accept exposure.

Section 6: The Calculator — Estimate Your Firm’s TCOR

Step 1: Calculate Baseline

Direct:

- Premium

- Uninsured exposure

Indirect:

- Error remediation

- Partner time

- Incident response

Opportunity:

- Lost RFP revenue

- Pricing penalties

- regulated sector procurement barriers

Step 2: Calculate Governance Scenario

Adjust:

- Premium with governance credit

- Remove uninsured exposure

- Reduce remediation by 60–70% (GAS Executive Edition benchmark)

- Add PBS implementation ($85K Year 1; $47K maintenance thereafter)

Step 3: ROI

(Net savings ÷ Implementation cost) × 100

Typical modeled range: 600–1,900% ongoing return.

Payback: 4–7 weeks.

The full TCOR calculator and implementation roadmap are detailed in the Governance Artifact System series, available on Amazon. The [GAS Production Edition] (affiliate link) is the primary reference for TCOR implementation. See the Recommended Resources section above for full details.

This article is the entrance ramp.

FAQ: Total Cost of Risk AI

1. What is the total cost of risk AI?

Total cost of risk AI is the full financial exposure created by AI use, including premiums, uninsured losses, compliance costs, and remediation expenses. The concept builds on traditional Total Cost of Risk (TCOR) models used in enterprise risk management. Source: https://www.milliman.com/en/insight/how-to-reduce-total-cost-of-risk-using-artificial-intelligence-and-machine-learning

2. How do you calculate the total cost of risk AI?

A simplified model is: Premiums + (Deductibles × Incident Probability) + Governance Costs − Risk Reduction. This adapts the traditional TCOR framework used by insurers and risk analysts.

3. Why isn’t AI risk fully covered by insurance?

Many insurers now include AI exclusions, stricter underwriting requirements, or narrower professional liability definitions because generative AI introduces new liability risks.

(This is the verified Insurance Business Canada article containing the Berger quote and directly supports the Q3 answer on AI exclusions becoming standard.)

4. How do AI errors increase the total cost of risk?

AI errors can trigger rework, client disputes, legal claims, regulatory investigations, and reputational damage—significantly increasing the total cost of risk.

5. Does AI governance reduce the total cost of risk AI?

Yes. Governance frameworks that document human oversight, validation procedures, and audit trails can reduce claim probability and improve insurability.

Reference: NIST AI Risk Management Framework. https://www.nist.gov/itl/ai-risk-management-framework

6. How does regulation affect the total cost of risk AI?

New regulations such as the EU AI Act and emerging AI liability rules increase documentation and accountability requirements. Non-compliance can result in fines, investigations, and higher insurance costs.

7. Which firms face the highest AI risk exposure?

Professional services firms—including legal, consulting, financial advisory, healthcare consulting, and technology firms—face the highest liability exposure because they rely on expert judgment.

8. Can the total cost of risk AI affect firm valuation?

Yes. Weak AI governance can reduce investor confidence, create regulatory exposure, and lead to valuation discounts during due diligence or acquisitions.

9. What is the fastest way to lower AI risk exposure?

Conduct an AI usage audit, review insurance exclusions, implement human-oversight controls, and document governance procedures.

10. Why is the total cost of risk AI often underestimated?

Because indirect costs—lost contracts, regulatory exposure, legal fees, premium increases, and brand damage—are often hidden from traditional risk calculations.

11. What is the difference between AI exclusions and affirmative AI coverage?

AI exclusions remove coverage for AI-related claims. Affirmative AI coverage explicitly confirms protection for AI-assisted work, usually requiring documented governance and oversight controls.

12. How does the Governance Artifact System reduce TCOR?

The Governance Artifact System (GAS) provides structured documentation, audit trails, and PBS governance protocols that help reduce claim probability and support affirmative AI coverage. Learn more in the GAS Production Edition: https://www.amazon.com/dp/B0GMBHTT5X

The Governance Artifact System™ — Executive Edition

By John Cosstick

Conclusion — The Cost of Waiting

Every month, without governance costs between $70K and $175K in avoidable TCOR exposure (scenario-based modeling).

That isn’t theoretical.

It’s arithmetic.

Being uninsurable isn’t just expensive. It’s existential.

You lose contracts.

You compress valuation.

You limit partner exits.

You repel top talent.

The real question isn’t:

“Can we afford to implement PBS?”

It’s: “Can we afford another month without it while competitors secure affirmative coverage and win the RFPs we’re excluded from?”

The total cost of risk AI is already on your balance sheet.

The only variable left is whether you measure it.

About the Author & Disclosures

John Cosstick is Founder-Editor of TechLifeFuture.com and winner of the 2024 BOLD Award for Open Innovation in Digital Industries. He is a former banker, accountant, and certified financial planner.

He is now a freelance journalist and author. John is a member of the Media Entertainment and Arts Alliance (Union). You can visit his Amazon author page by clicking HERE.

Disclosures

At TechLifeFuture, every article undergoes a multi-step fact-checking and citation audit process. We verify technical claims, research findings, and statistics against primary sources, authoritative journals, and trusted industry publications. Our editorial team adheres to Google’s EEAT (Expertise, Experience, Authoritativeness, and Trustworthiness) principles to ensure content integrity. If you have questions about any references used or would like to suggest improvements, please contact us at [email protected] with the subject line: Citation Feedback.

Affiliate disclosure:

We are a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for us to earn fees by linking to Amazon.com and affiliated sites. If you click on an Amazon link and make a purchase, we may earn a small commission at no extra cost to you.

General disclaimer:

All analyses are provided for informational and educational purposes only and do not constitute legal, financial, or professional advice. Readers should consult qualified professionals before acting on any information contained in this article. Information current as at 8 March 2026 (AEST).

Compliance Block

Disclosure v3: This article reflects independent analysis by TechLifeFuture.com. References to Governance Artifact System (GAS) publications are disclosed as related intellectual property of the author.

AI Assistance Statement: AI tools were used for research structuring and editorial support. All proprietary modeling data is based on GAS internal research and scenario benchmarks.

Creative Commons: Licensed under Creative Commons Attribution 4.0 International (CC BY 4.0), unless otherwise noted.

Change Log: Version 1.0 — March 2026 — Initial publication draft.

Patent Notice: Patent pending AU 2025220863 | PCT/IB2025/058808. Intelligence-layer discussion only. No system architecture, machinery, or execution mechanism disclosure included.

Insurance/regulatory references

- How Insurance Policies Are Adapting to AI Risk

https://www.hunton.com/insights/publications/how-insurance-policies-are-adapting-to-ai-risk - Munich Re aiSure™ AI Insurance Solution

https://www.munichre.com/en/solutions/for-industry-clients/insure-ai.html - Munich Re aiSure™ FAQ Page (Additional Context)

https://www.munichre.com/en/solutions/for-industry-clients/insure-ai/faq.html - Munich Re AI Insurance Whitepaper (Context and Market Trends)

https://www.munichre.com/en/solutions/for-industry-clients/insure-ai/ai-whitepaper.hsb.html - EU AI Regulation and Insurance Context

https://automation-solutions.munichre.com/rs/198-IDM-109/images/AI%20transformation%20in%20insurance%20underwriting%20ebook%20FINAL.pdf?version=0 - Emerging Affirmative AI Coverage (Armilla& Lloyd’s)

https://natlawreview.com/article/affirmative-artificial-intelligence-insurance-coverages-emerge - Michael Berger, Head of AI Insurance, Munich Re. Speaking at the National Insurance Conference of Canada. Insurance Business Canada, October 2025. https://www.insurancebusinessmag.com/ca/news/technology/insurers-brace-for-silent-ai-exposures-as-underwriting-methods-evolve-552670.aspx