Executive Summary

The question facing every boardroom, partner meeting, and platform leadership team in 2026 is no longer whether artificial intelligence will reshape professional advice. That question is settled. The harder question — the one that determines who is sued, who is uninsurable, and who is fined — is who bears liability when AI-generated advice causes loss.

Courts on three continents are answering it the same way: the organisation that deployed the system carries the consequences, not the system. Air Canada cannot hide behind its chatbot. UnitedHealth cannot hide behind NH Predict. Workday is being told it cannot hide behind the claim of being “just the vendor.” The legal direction of travel is unmistakable. Regardless of how an output was produced, courts are treating it as an organisational output.

This article is written for the three populations of readers who carry that weight in practice: directors with fiduciary duties extending into algorithmic territory they may not yet fully understand, licensed professionals who must maintain the same standard of care despite the arrival of generative tools, and platform operators sitting between the vendors above them and the users below.

Each faces a new failure mode – synthetic compliance – in which organisations use the same AI systems they seek to govern to generate, reconstruct, or paraphrase the governance evidence intended to demonstrate oversight. The volume of policies, charters, risk registers and assurance memoranda has multiplied. The verifiability of any of them has not.

What follows examines the legal foundations, the landmark cases now defining the duty, the regulatory expectations across professions, the duties of directors and platform operators, and the governance and insurance posture required to remain defensible — and insurable — through the Insurance Cliff that is now hardening across the global underwriting market.

The Rise of AI as a “Co-Advisor” in Professional Practice

A decade ago, the phrase “AI in professional services” described a research interest. Today it describes a workflow. Lawyers compress hundreds of pages of discovery into actionable summaries through large language models. Doctors triage radiology images with classifiers that flag findings their human eyes would have caught on a slower day.

Financial advisers run client scenarios through robo-portfolio tools that rebalance in milliseconds. Accountants reconcile ledgers through systems that no longer feel like software at all — they feel like junior staff.

The productivity gain is real. So is the unit-economics gain. So is the speed at which capability scales across a firm. What also scales is the surface area of exposure. Every AI-assisted output that touches a client is an output that can be challenged in court, in front of a regulator, or by an insurer at renewal. The firm gets the speed; the firm also gets the duty of care that follows.

The frame this article uses is straightforward. AI in professional advice is not a replacement for the professional. It is a co-advisor — capable, fast, occasionally wrong in ways that are confidently expressed and difficult to detect after the fact. Co-advisors require supervision. Where they are not supervised, liability accumulates silently until it is realised in a claim, a complaint, or a denied renewal.

The Governance Illusion

Policies Are Aspirational — They Are Not Proof

Every professional governance framework starts with a policy document. That is fine. Policies articulate intent, establish responsibility, and set the parameters for acceptable behaviour. But there is a category error that has become surprisingly common in AI governance: the conflation of policy with proof.

A policy that says your organisation will not use AI systems in high-stakes decisions without human review tells you nothing about whether that human review actually occurs. A data governance register that lists your active AI tools tells you nothing about the shadow tools that have entered through individual licence accounts, embedded integrations, and browser-level add-ons. An attestation signed by a compliance officer tells you that a compliance officer signed something — it does not tell you that the thing signed corresponds to operational reality.

Registers carry their own fragility. The teams being assessed typically maintain these records, which creates an obvious incentive to present themselves favourably. Organisations also frequently compile them retrospectively in the week before an audit rather than maintain them contemporaneously. And they are rarely subject to independent verification against system telemetry, API logs, or usage records that would confirm the register’s accuracy.

Attestation exercises, particularly under volume pressure, drift toward checkbox compliance. When an organisation must produce AI governance attestations across dozens of systems before a procurement deadline, the incentive is to produce clean documentation quickly — not to surface inconvenient gaps. Boards and audit committees see governance activity presented in polished slide formats. What they rarely see is any evidence of governance authenticity: any signal that would allow them to distinguish genuine oversight from well-formatted theatre.

What boards typically see:

Policy documents · Risk registers · Attestation sign-offs · Oversight committee minutes

What boards rarely see: Independent verification · Tamper-evident logs · Chain-of-custody for artefacts · Telemetry-grade evidence

The Synthetic Compliance Problem

When the AI Systems Write Their Own Governance Evidence

There is a term that does not yet appear in ISO/IEC 42001 guidance, in the EU AI Act recitals, or in the NIST AI Risk Management Framework — but it needs to. That term is synthetic compliance: governance evidence that is generated, reconstructed, or paraphrased by the same AI systems it purports to govern.

The definition matters because it identifies a failure mode that sits upstream of any other governance problem. If the evidence base itself is produced by the system under review — or by a closely related AI system operating without independent oversight — then every subsequent audit, assurance, and attestation process is built on a foundation that cannot be independently tested.

The governance documentation may be technically accurate, competently written, and internally consistent. It may also be entirely disconnected from operational reality.

Four Failure Modes

First: AI-drafted policies recycled without substantive review

Generative AI tools make it straightforward to produce a responsible-use policy, an AI risk register, or a supplier due diligence questionnaire in under an hour. When that output is accepted without material revision and without verification against the actual technical architecture of the system being described, the result is documentation that bears the organisation’s name but reflects no organisational knowledge of its own AI estate.

Second: Reconstructed audit trails written after incidents

In a post-incident review, there is a powerful incentive to produce documentation that shows the organisation’s governance processes were operating correctly — even when they were not. AI drafting tools lower the friction for producing that documentation retrospectively. The trail looks plausible. The timestamps may even be fabricated or selectively applied. An independent auditor who can only review the documentation has no mechanism for detecting this.

Third: Teams often copy and paste risk assessments between unrelated systems

Illustrative example: an organisation completing AI risk assessments across a portfolio of tools may reuse substantially the same narrative across different systems, substituting product names but retaining the underlying risk language. Each assessment appears complete. None accurately reflects the specific risk profile of the system it purports to describe.

Fourth: Governance theatre

Well-rehearsed narratives — terms like ‘human-in-the-loop’, ‘model cards’, ‘ethical AI review’ — are deployed with confidence in procurement responses and board presentations, with no independently verifiable evidence underneath. The vocabulary is correct. The substance is missing.

ISO/IEC 42001 implementation will expose this gap — not immediately, but progressively. As auditors become more sophisticated in their assessment of AI governance systems, they will begin asking not just whether artefacts exist, but who generated them, how they generated them, and whether independent controls govern the generation process itself. Organisations that have built their governance programmes on synthetic compliance will face a reckoning when auditors examine those questions with real rigour.

This is a procurement and audit problem before it becomes a regulatory one. Organisations that get ahead of it will have a material advantage — not only in demonstrating compliance, but in being able to defend governance decisions when they are actually tested.

Legal Foundations: Why AI Does Not Remove Human Responsibility

Three legal concepts do most of the work in this article: negligence, malpractice, and fiduciary duty. None of them has been altered by the arrival of generative tools. All three apply to AI-assisted work just as they apply to work produced entirely by a human professional.

Negligence asks whether the standard of care was met. The standard does not bend to accommodate the use of a tool. A lawyer who files a brief containing fabricated citations because the underlying model hallucinated them has not met the standard. A clinician who relies on an AI summary that omits a contraindication has not met the standard.

The tool is part of the workflow; the workflow remains the professional’s.

Malpractice extends the same logic into licensed professions. The advice given is the advice given, regardless of who or what generated the draft. The professional is accountable for the advice that leaves their office under their name.

Fiduciary duty is the most quietly consequential of the three for directors. It does not stop at the boundary of the systems the board chose to deploy. A board that adopts an AI-enabled service into the client-facing chain of the business has folded that service into the duties it owes. The board cannot delegate fiduciary duty to a vendor’s terms of service.

The unifying principle, plainly stated, is this: AI has no legal personhood. There is no entity called “the AI” to be sued, fined or struck off. Liability flows upward — to the professional, to the deploying organisation, to the directors who oversee it.

Where governance evidence is itself produced by the same system it purports to oversee — the synthetic-compliance failure mode — the defence collapses inward. There is nothing independent left to point to.

Why Traditional Governance Evidence Breaks Down

The Architecture of Modern AI Use Is Incompatible With Legacy Oversight

The governance frameworks most organisations are working from were designed for a different kind of technology estate. They assume that AI tools are discrete, identifiable, and centrally procured — that there is a list of systems, and that list is accurate. That assumption has not reflected operational reality for at least three years.

AI tools are now distributed across business units in ways that have no historical parallel. Finance teams are running expense categorisation and anomaly detection through embedded AI layers in their ERP systems. HR functions are using AI-assisted candidate screening tools procured independently of central IT.

Marketing and legal teams are using generative AI tools accessed through individual or departmental subscriptions. The IT department may know about none of this — or it may know about some of it, from some of those teams, some of the time.

Shadow AI

AI tools operating outside formal governance oversight are no longer an edge case. It is the default operating condition for a large proportion of professional services organisations. Usage that bypasses governance registers is not confined to rogue actors; it is the predictable consequence of AI capability being accessible through consumer-grade tools that require no technical deployment.

Agentic workflows

Agentic workflows add another layer of complexity. When AI systems execute multi-step actions across multiple systems — drafting, routing, approving, and filing in sequence — there is frequently no single point of accountability in the process. Each step may be auditable in isolation. The chain of custody across the whole workflow is typically unrecorded, and responsibility for any single decision within that workflow becomes genuinely difficult to attribute.

API integrations produce fragmented logs distributed across multiple vendor systems, with no single party responsible for reconciling them into a coherent audit record. Frequency-of-use telemetry — knowing that a model was queried 847 times in a given week — answers a fundamentally different question from governance accountability.

It tells you the system was used. It does not tell you whether it was used in accordance with its stated governance parameters, whether human review occurred at the required decision points, or whether the outputs were acted on without the oversight the policy required.

Why legacy governance frameworks fail the modern AI estate:

- Distributed AI tools sit across business units with no central inventory

- Shadow AI is now embedded in finance, HR, marketing, and legal workflows

- Agentic workflows execute across systems with no single accountability point

- API integrations leave fragmented logs no one is responsible for reconciling

- Usage telemetry answers a different question from governance accountability

Landmark Case Signals: What Courts Have Already Decided

Three cases now anchor the legal direction of travel. Each was decided or progressed substantially between 2024 and 2026. Together, they cover the consumer-service, employment and healthcare-coverage layers of the AI economy.

Moffatt v. Air Canada (2024)

In February 2024, the British Columbia Civil Resolution Tribunal held Air Canada liable for misleading information provided to a passenger by its website chatbot. The passenger, recently bereaved, had relied on the chatbot’s description of the airline’s bereavement-fare policy when booking.

The information was wrong. Air Canada’s defence was striking: it argued the chatbot was a separate legal entity responsible for its own actions. The tribunal rejected the argument outright. The chatbot was part of the airline’s website; the airline was the service provider; the duty of care applied. Negligent misrepresentation was made out.

The case has been cited internationally ever since because the defence Air Canada attempted is the defence almost every organisation deploying a public-facing AI tool has been tempted to rely on. The tribunal closed that path.

Mobley v. Workday (2024–2025)

In July 2024, the United States District Court for the Northern District of California allowed claims against Workday — not against the employers using Workday’s tools, but against Workday itself — to proceed beyond a motion to dismiss. The plaintiff alleged that Workday’s AI-powered applicant-screening systems produced a disparate impact on candidates over forty, on grounds of race and on grounds of disability. The court declined to characterise Workday as an “employment agency” but accepted that it could be treated as an “agent” of the employers using its tools, exposing the vendor itself to direct liability under federal anti-discrimination law.

In May 2025, the court conditionally certified the age-discrimination claim as a collective action potentially covering millions of applicants. The Equal Employment Opportunity Commission filed an amicus brief supporting the agent theory. The signal to AI vendors is clear: a vendor cannot fully wall itself off from how its tools function in the field.

Estate of Lokken v. UnitedHealth Group (2023–ongoing)

In Minnesota, the families of two deceased Medicare Advantage beneficiaries are pursuing UnitedHealth, UnitedHealthcare and the Optum subsidiary now operating as Home & Community Care over the alleged use of an AI tool — nH Predict — to terminate post-acute care coverage prematurely. The plaintiffs allege the algorithm was used to override clinical judgment, that error rates were known to the insurer, and that the result was discharges that caused real harm.

In February 2025, the court allowed claims for breach of contract and breach of the implied covenant of good faith and fair dealing to proceed. In March 2026, a federal magistrate judge ordered broad discovery into how the tool was implemented and used inside the business. The insurer’s position — that nH Predict is a care-support guide rather than a coverage-decision tool — will now be tested against the documentary record.

The TLF read across the three cases

The “AI did it” defence is being rejected by tribunals, federal courts and discovery orders alike. Each case turns, in its own way, on the same point: an organisation that deploys an AI system in a chain of decisions affecting people remains responsible for the outputs of that chain.

Where that organisation cannot produce independent, contemporaneous, machine-verifiable evidence of how the system was supervised — where the only governance artefacts on hand were drafted by, or in lockstep with, the very system being defended — the defence runs out of ground to stand on.

The Shift Toward Verifiable Governance

Defining What Verification Actually Requires

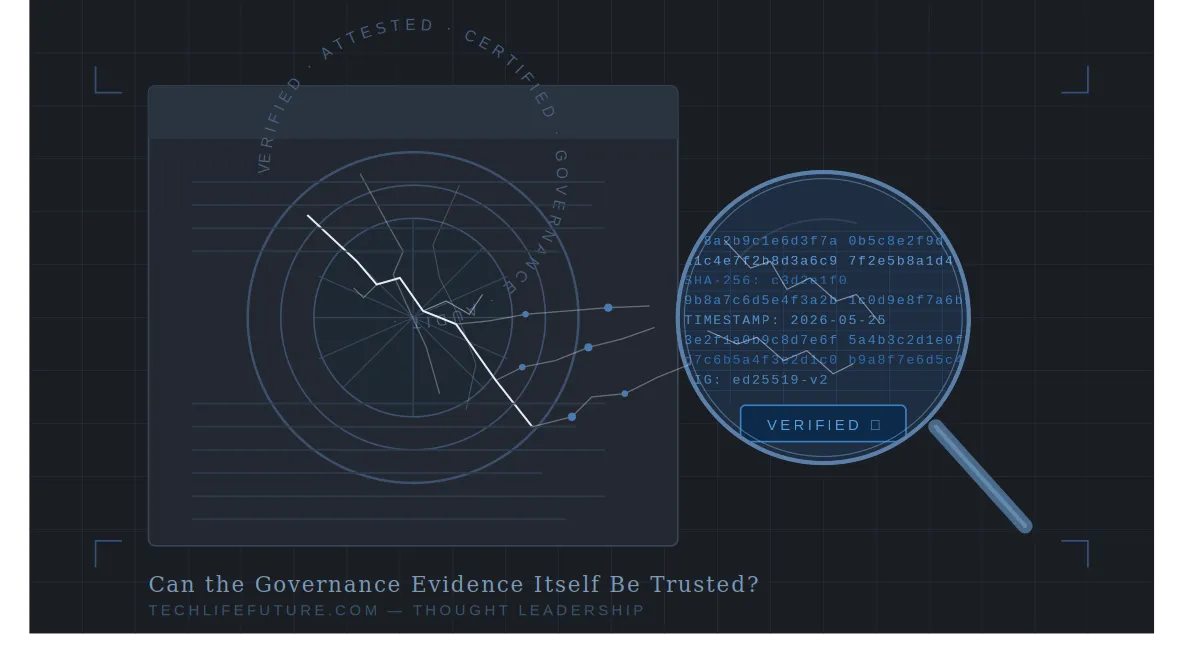

The word verifiable is used frequently in AI governance discussions. It is used infrequently with precision. For governance evidence to be genuinely verifiable — to stand up to the scrutiny of an independent auditor, an insurer’s claims team, or a procurement panel with real technical capability — it needs to satisfy four properties.

Independent.

The evidence must be generated or validated by a process that is not controlled by the entity being governed. Evidence that is produced, stored, and retrieved entirely within the same system being assessed offers no meaningful independence.

Tamper-evident.

Any modification to the record – after the fact, for any reason – must be detectable. This is not an unusual requirement; it is the standard applied to financial records and legal evidence. AI governance artefacts are not currently held to this standard in most organisations.

Time-bound.

The evidence must be anchored to a specific moment — not a reporting period, not a retrospective reconstruction, but a verifiable timestamp that can be confirmed against an independent reference.

Attributable.

Every governance action — every review, approval, or exception — must be attributable to a specific human or system. Anonymous sign-offs and collective committee endorsements are not governance evidence; they are governance assertions.

Immutable Records and Why They Matter to Insurers

Immutable records — records that cannot be altered after creation without that alteration being detectable — are the technical floor for verifiable governance. Insurers understand this concept from the marine, property, and financial contexts where chain-of-custody evidence has been required for decades. The emerging question in AI governance is whether the same standard can be applied to AI system behaviour records — and if so, what infrastructure is required.

The distinction between telemetry-grade evidence and narrative evidence is important here. A narrative governance report — a written account of what the oversight process involved — is useful as a summary. It is not independently testable. Telemetry-grade evidence — structured logs, cryptographically signed records, immutable event sequences — can be tested. An auditor can ask specific questions about specific events and receive verifiable answers, rather than accounts.

Cryptographic attestation is emerging as the new floor for serious AI deployments — a method by which specific claims about AI system behaviour (that a human reviewed a decision before it was executed; that a model version was the one specified in the governance register; that a specific output was generated at a specific time) can be bound to a verifiable proof. This is not a theoretical concept; it is an extension of certificate-based trust models that are already standard in enterprise security.

The legal-evidence concept of chain-of-custody — the documented, unbroken sequence of possession and handling that makes physical evidence admissible — has a direct analogue in AI governance. If the provenance trail of a governance artefact cannot be established, that artefact cannot be relied upon in a high-stakes dispute. Organisations that build chain-of-custody principles into their AI governance architecture now will not need to reconstruct them under pressure later.

The Governance Artifact System™ (GAS™) — Conceptual Note

One emerging direction in this space is the Governance Artifact System™ (GAS™) — a framework approach built around the principle that governance evidence should be generated, timestamped, and stored in a manner that satisfies the four verifiability properties above.

The Edit Delta™ concept, for example, produces a measurable, time-bound signal that captures human contribution to AI-assisted outputs — a signal a third party can examine and verify, rather than a narrative a team has composed about its own processes. This is one illustration of where the field is heading; the principles apply regardless of which specific infrastructure an organisation selects.

Three Circles of AI Accountability

The liability falling out of these cases does not land in one place. It lands in three, and the failure modes for each are different.

Liability risks in critical sectors demonstrate why narrative governance is insufficient. The following Stanford HAI briefing summarises how healthcare deployments now translate into civil liability.

The AI Developer (vendor)

Vendors have historically relied on contract disclaimers, indemnity-cap clauses and shrink-wrap language to define the perimeter of their exposure. Mobley v. Workday weakens that perimeter. Where a vendor’s tool operates as the decision-shaping mechanism inside a customer’s regulated process, the vendor’s role can be characterised as agency for the deployer, and product-liability-style claims become plausible.

The synthetic-compliance failure mode appears at the vendor layer when assurance documentation — model cards, bias audits, fairness statements — is generated by, or trivially reused from, the vendor’s own systems with no independent verification.

The Deploying Organisation (platform or operator)

This is the strongest accountability link, and it is also the most exposed. The deploying organisation controls the integration, controls the client relationship, and controls the human-oversight design — or its absence. Air Canada sits here. UnitedHealth, on the plaintiffs’ case, sits here.

The synthetic-compliance failure mode at this layer is the most damaging: accepting an AI-drafted responsible-use policy, an AI-drafted risk register or an AI-drafted compliance attestation as evidence of governance, when in practice the same systems being governed are the systems doing the drafting.

The Licensed Professional

Lawyers, doctors, financial advisers, accountants and engineers operate within duties of competence, confidentiality and supervision that long predate generative AI and have not been softened by it. The professional at this layer is exposed wherever they engage in governance theatre — labelling a workflow “human-in-the-loop” without any verifiable record of cognitive effort by the human. Edit Delta™ — a measurable, time-bound signal capturing what the human actually changed — is the metric this article returns to in the mitigation framework because it is the answer to that exposure.

The three circles overlap. A single AI-driven decision often touches all three at once. When something goes wrong, the question is rarely which circle was at fault. The question is which circle has the verifiable evidence to demonstrate that it did its part.

The Insurance and Procurement Reckoning

The Insurance Cliff — From Silent Coverage to Active Exclusion

For most of the past five years, AI risk has sat as an implicit element within professional indemnity and cyber insurance policies — not explicitly covered, not explicitly excluded, and therefore subject to a great deal of interpretive uncertainty when claims arose. That period is ending.

What the industry is now calling the Insurance Cliff describes the shift from silent AI coverage — where policies neither addressed AI use nor excluded it — to affirmative AI exclusions, where AI-related risks are explicitly excluded from standard cover unless the insured can demonstrate specific governance conditions.

From Policy Statements to Verifiable Evidence

Those conditions are not satisfied by producing a policy document. They are satisfied by producing verifiable evidence of the governance practices the policy describes.

Immediate Consequences for Professional Services Firms

The implications are significant and immediate for professional services firms, advisers, and regulated-sector organisations. A legal practice using AI-assisted drafting tools without verifiable human review records may find that an AI-related professional liability claim is excluded from its PI cover. An audit firm that cannot demonstrate chain-of-custody for AI-assisted working papers may face a coverage dispute. A financial advisory practice that has incorporated AI tools into advice processes without tamper-evident records of oversight may be exposed in a way it has not yet assessed.

Procurement Standards Are Tightening

Government and infrastructure procurement is moving in parallel. Tender documentation for public sector AI projects is increasingly requiring evidence of AI governance that goes beyond attestation — requiring governance frameworks that can be independently assessed, records that can be examined, and assurance processes with real accountability architecture. Organisations that cannot produce verifiable evidence will find themselves outside procurement panels that they previously qualified for without difficulty.

The Emerging Standard of Care

Professional liability implications extend to retired and practising advisers, lawyers, and auditors who have incorporated AI tools into their professional work. The standard-of-care question — whether a professional exercised appropriate oversight of AI-assisted outputs — will increasingly be tested against whether verifiable evidence of that oversight exists. Good intentions and plausible process descriptions will not, by themselves, satisfy that test.

Runtime Insurability Enforcement

Runtime insurability enforcement is an emerging concept worth noting: the prospect of AI governance systems that, rather than passively recording governance activity, actively condition system operation on governance preconditions being met — systems that will not execute certain actions unless specified oversight conditions are satisfied and can be verified in real time. This is at the development edge of the field, but it represents a logical extension of the principles above.

Regulatory Expectations: “Old Rules, New Tools”

Across the regulated professions, the regulatory line is the same, expressed in slightly different vocabulary. Existing obligations apply. AI is not an exception.

Financial Services — FINRA Notice 24-09

On 27 June 2024, the Financial Industry Regulatory Authority issued Regulatory Notice 24-09 to remind member firms that its rules and the federal securities laws apply to the use of artificial intelligence, including large language models and other generative AI, just as they apply to any other technology. The notice did not introduce new rules. It explicitly stated that the existing supervisory framework — including Rule 3110’s requirement for a reasonably designed supervisory system — extends to AI use. Firms cannot outsource their compliance obligations to the model.

Healthcare — malpractice and safety

Courts continue to apply the established standard: what would a reasonably careful clinician have done with this tool in these circumstances? The arrival of AI changes the answer to that question only by raising the bar. A clinician now bears the additional burden of understanding the tool’s known failure modes and accounting for them in care.

Legal Profession — ethics and confidentiality

Bar associations across multiple jurisdictions have aligned on the same posture: lawyers must supervise AI as they supervise nonlawyer assistants. Competent practice now requires an understanding of the technology’s limitations and potential failure modes. Confidentiality obligations extend fully to prompts, retrieval pipelines, and generated outputs. In addition, lawyers remain responsible for verifying AI-generated work product before it leaves the office, reflecting their continuing duty of supervision.

Board-level governance

Directors are expected to treat AI as a board-level risk category. That means documented oversight, periodic reporting, identifiable accountability for material deployments, and explicit linkage between AI risk and the firm’s insurance posture. A board that cannot demonstrate this is no longer in the position it was in five years ago. It is exposed.

What Happens Next

Five Forecasts for the 2025–2027 Window

The shift from governance documentation to verifiable governance evidence will not happen uniformly or all at once. But the direction is clear, and the timeline is compressed. These five forecasts describe where the field is heading — not as speculation, but as extensions of pressures already visible in the market.

Forecast 1: Machine-verifiable governance becomes the audit floor, not the leading edge.

What currently distinguishes the most sophisticated AI governance programmes — tamper-evident records, cryptographic attestation, provenance trails — will become the baseline expectation for ISO/IEC 42001 certification and regulated-sector procurement. Organisations that have not invested in this infrastructure will find themselves at the same disadvantage as those who were still using paper records when electronic audit trails became standard.

Forecast 2: AI ‘black box recorders’ enter procurement specifications.

By analogy with flight data recorders — which capture a continuous, tamper-evident record of system state — procurement specifications for high-stakes AI deployments will begin requiring continuous governance telemetry as a contractual condition. The requirement will be framed in terms of audit defensibility and incident investigation capability, not innovation.

Forecast 3: Continuous compliance telemetry replaces annual attestation cycles.

Annual attestation — the model in which an organisation attests to its governance practices at a point in time — is fundamentally misaligned with the continuous and adaptive nature of AI system behaviour. The pressure from insurers, auditors, and procurement panels will drive the adoption of continuous monitoring architectures that can demonstrate governance status at any point, not just at attestation intervals.

Forecast 4: Runtime governance enforcement.

Systems will increasingly be designed to refuse to act when governance preconditions are not met — when a human reviewer has not confirmed a required oversight step, when an AI tool is not on the verified register, or when a decision type triggers a mandatory review that has not occurred. Governance will shift from a recording function to an enforcement function.

Forecast 5: Evidence-linked AI assurance frameworks emerge alongside ISO/IEC 42001.

The ISO/IEC 42001 standard provides an excellent framework for AI management systems. What it does not yet do — in its current form — is mandate the kind of verifiable evidence architecture described in this article. Third-party assurance frameworks that go further, requiring evidence-linked verification rather than documentation-based attestation, will emerge in the next 18 months and will set a new market standard for governance credibility.

The strategic question for boards through 2026–2027:

Can your organisation produce, on short notice, verifiable evidence that your AI governance framework operated as described — for any system, at any point in time, in a form a sceptical third party could independently assess? If the answer is uncertain, the gap is not a compliance gap. It is a risk architecture gap.

Duties of Directors and Platform Operators

The instinct of many boards has been to receive AI governance the way they have received other emerging risk categories: through polished slide decks, retrospective dashboards and thicker assurance memoranda from management. That posture no longer survives the duty of care.

Fiduciary duty now unambiguously extends into algorithmic territory. A board cannot discharge that duty through narrative governance alone. The set of things a board must be able to identify, document and revisit has grown:

- Every client-impacting AI deployment in the business is named and owned by someone in management.

- Validation and monitoring evidence for each material deployment — not a vendor brochure, but a contemporaneous, independent record.

- Human-oversight pathways for each system, with a clear answer to the question of who reviews what, when, and with what evidence of effort.

- Bias, privacy, and safety controls, including the conditions under which the system would be paused or rolled back.

- An explicit map between the firm’s AI exposure and its insurance coverage — E&O, professional indemnity, cyber, D&O — so that nothing material sits in the gap.

The deeper directorial obligation is the one that does not show up in management’s slides: independent verifiability. The artefacts on which the board relies must not have been generated by the same systems they purport to govern. If they were, the board would not have been governed; it has been narrated to.

Professional Ethics: How Advisors Must Use AI Safely

The ethical obligations of licensed advisors translate into AI use cleanly, once translated honestly.

The duty of competence now includes understanding what the AI tool in use cannot do, where it fails, and how to recognise the failure before it reaches the client. Confidently presented hallucinations are the defining clinical hazard of large language models. A competent practitioner treats them as such.

The duty of confidentiality applies in full to inputs as well as outputs. A prompt that contains client information, a retrieval pipeline that touches privileged material, a draft that is paraphrased through a third-party model — each is a confidentiality event. The professional retains responsibility for the perimeter.

The duty of supervision is the duty that synthetic compliance most aggressively erodes, and it is therefore the duty that matters most. Every AI-generated artefact entering the professional’s output chain requires real, evidence-based human review. The framing TLF recommends is plain: AI is a junior colleague, not a senior advisor. A junior colleague’s work is checked before it leaves the building. So is the AI’s.

Governance & Risk Mitigation Framework (TLF Standard)

A defensible posture against the liability landscape described in this article rests on five layers. They are intentionally ordered from the strategic to the operational.

Legal scholars increasingly agree that the next phase of algorithmic accountability will rely heavily on verifiable telemetry and immutable evidence. The Stimson Center panel below frames the transition.

1. Policy & Process

A formal AI use policy is the precondition for everything else. The policy must name the approved tools, the gating process for new ones, and the prohibited uses. Critically, the policy itself must not be a synthetic artefact: a compliance document drafted by the same systems it purports to govern is not a policy; it is governance theatre. Where AI assistance is used in drafting, the human authorship and editorial chain must be recorded.

2. Model Governance

Approved tools must be validated before deployment and monitored after it. Accuracy testing, bias audits, incident logging and explicit escalation paths form the operational core. Vendor attestations are inputs to model governance, not substitutes for it; independent verification is required where the deployment is client-impacting.

3. Human Oversight

Mandatory human-review steps must be designed into every high-stakes output chain — and the review must be evidenced. This is where Edit Delta™ does its work. By capturing what the human actually changed, in what time window and with what reasoning, Edit Delta™ converts “human-in-the-loop” from an assertion into a measurable, retrievable record. It is the answer to the synthetic-compliance failure mode at the operational layer.

4. Skilling & Training

Continuing professional development must include AI literacy specific to the tools the firm has approved. Documented learning pathways are not a nice-to-have; they are evidence for regulators, for insurers, and for courts — that the firm took its duty of competence seriously across its workforce.

5. Insurance Strategy

The Insurance Cliff is no longer a forecast. Underwriters are hardening positions, conditioning renewals on demonstrable governance, and writing affirmative AI exclusions into Errors & Omissions, professional indemnity and cyber towers. Defending a renewal requires evidence that aligns with the underwriter’s questions before they are asked. The firms that survive the cliff are the firms whose immutable governance records map cleanly onto the underwriter’s view of risk.

Future Outlook

The direction of travel across the United Kingdom, the European Union, the United States and Australia is consistent: away from generic AI principles and toward sector-specific liability rules, certification schemes and insurability linkages. The EU AI Act has already established the template for risk-tiered regulation. The UK and Australia are following with sector-by-sector codes. The United States, in the absence of a single federal framework, is moving through the courts and through state-level action.

Three signals will harden over the next eighteen months. First, audit expectations will sharpen: regulators will increasingly ask for evidence of independent verification, not vendor attestation. Second, certification schemes will become a precondition for participation in regulated procurement, not a marketing differentiator. Third, insurability will become the practical limit on AI deployment — the firms that can produce telemetry-grade evidence will be insurable risks; the firms that cannot will not.

Firms that adopt the governance posture early will not only stay insurable; they will price into the market at lower premiums and win contracts that closed competitors cannot. The advantage compounds.

Frequently Asked Questions

Q1. Who is liable when AI gives bad advice?

The organisation deploying the AI — not the bot — remains responsible. Tribunals and courts now treat AI outputs as organisational outputs.

Source: American Bar Association — https://www.americanbar.org/groups/business_law/resources/business-law-today/2024-february/bc-tribunal-confirms-companies-remain-liable-information-provided-ai-chatbot/

Q2. Can a company argue “the chatbot did it”?

Courts and tribunals are rejecting that defence. Companies remain responsible for the accuracy of all AI outputs on their public-facing channels.

Source: The Guardian — https://www.theguardian.com/world/2024/feb/16/air-canada-chatbot-lawsuit

Q3. Can AI vendors be sued?

Yes. In Mobley v. Workday, a US federal court has allowed claims against the vendor itself to proceed under an “agent” theory of liability.

Source: Seyfarth Shaw — Mobley v. Workday agent-theory ruling. https://www.seyfarth.com/news-insights/mobley-v-workday-court-holds-ai-service-providers-could-be-directly-liable-for-employment-discrimination-under-agent-theory.html

Q4. Does AI change malpractice rules?

No. Professionals remain responsible for verifying AI-assisted advice. The standard of care does not bend to accommodate the use of a tool.

Source: New England Journal of Medicine — https://www.nejm.org/doi/10.1056/NEJMhle2308901

Q5. Does AI change financial-advice rules?

No. FINRA Notice 24-09 confirms that compliance obligations are technology-neutral and remain identical with or without AI.

Source: FINRA Regulatory Notice 24-09 — https://www.finra.org/rules-guidance/notices/24-09

Q6. Does PI insurance cover AI-related mistakes?

Usually yes, but insurers increasingly expect demonstrable governance and human oversight, and are writing affirmative AI exclusions where they do not see it.

Source: Informed PC — AI liability commentary https://informedpc.com.au/

Q7. Is there an AI liability gap?

Partially. European analysis shows real gaps for opaque AI systems, which the EU AI Act and accompanying liability instruments are intended to close.

Source: Eversheds Sutherland — AI liability commentary, https://www.eversheds-sutherland.com/global/en/what/articles/index.page?ArticleID=en/Global/ai-liability-part-1

Q8. What are the risks of AI hiring tools?

Bias, discrimination and legal exposure for both vendors and employers. Disparate-impact claims against AI screening tools are now active in US federal court.

Source: ClassAction.org — https://www.classaction.org/ai-discrimination-lawsuits

Q9. How can firms reduce AI liability?

Policy, model governance, evidence-based human oversight, training and insurance-aligned record-keeping. The TLF mitigation framework above sets out each layer.

Source: Mayer Brown — https://www.mayerbrown.com/en/insights/publications/2024/07/finra-reminds-members-of-regulatory-obligations-when-using-generative-artificial-intelligence-ai-and-large-language-models

Q10. Should AI be a board-level risk category?

Yes. Directors must oversee AI as part of their fiduciary duty, with documented evidence rather than narrative assurance.

Source: Eversheds Sutherland — https://www.eversheds-sutherland.com/global/en/what/articles/index.page?ArticleID=en/Global/ai-liability-part-1

Authority Reference Links

Primary source documents referenced throughout this article:

- ISO/IEC 42001 — https://www.iso.org/standard/81230.html

- EU AI Act — https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32024R1689

- OECD AI Principles — https://oecd.ai/en/ai-principles

- Australian AI Ethics Framework — https://www.industry.gov.au/publications/australias-artificial-intelligence-ethics-framework

Conclusion — AI Professional Advice Liability

The AI capability curve is steep. The accountability curve, which sits beneath it, is steeper. Human responsibility for AI-generated work is not retreating. It is intensifying — across courts, across regulators and across underwriters — because the alternative is a world in which no one is accountable for anything.

The winners over the next cycle will be the firms that adopt AI responsibly, transparently and with documented governance that is genuinely independent of the systems it governs. The losers will be the firms that mistook the volume of their governance documentation for its verifiability.

The question with which this article opened — who is on the hook when AI-generated advice goes wrong? — has a short answer and a long one. The short answer is: the organisation that deployed the system. The long answer is the work this article has just described.

About the Author

John Cosstick is a writer, author, and the Founder-Editor of TechLifeFuture.com, drawing on deep prior experience across banking, financial planning, and accounting. A Retired Certified Financial Planner and retired Fellow of the Institute of Public Accountants (FIPA), he is also a partner and minor shareholder in Mindhive.ai and maintains a portfolio of patent applications pending before IP Australia and the World Intellectual Property Organization (WIPO) covering AI governance, cryptographic verification and insurability frameworks. His work has been recognised internationally: in 2024, he won the BOLD Award for Open Innovation in Digital Industries, and in 2026, the BOLD Awards VII InsurTech category for AIMS Governance.

Earlier in his career, he served as a bank compliance manager and has since contributed to the UK Money and Pensions Service Debt Review and UN AI for Good initiatives. Writing from Melbourne, Australia, John focuses on AI governance, professional liability and the insurability of AI-enabled professional services. A preview of his recent book, The Governance Artifact System — How to Secure Professional Liability Insurance in the AI Era, is available on Amazon: view the preview here.

AI Assistance Disclosure

Portions of this article were AI-assisted in drafting and were subsequently human-reviewed and edited for accuracy, regulatory currency, and compliance with the TLF Editorial Standard v3 zero-fabrication requirement.

Legal and Professional Disclaimer

This article reflects AI, regulatory and professional-services practices as at 27 May 2026 (AEST). Readers should confirm whether subsequent guidance has been issued by their professional bodies.

Content on TechLifeFuture.com is for educational and informational purposes only and does not constitute legal, accounting or financial advice. Some links may be affiliate or referral links (including Amazon, Educative.io, and Mindhive.ai). If you purchase through these links, TechLifeFuture.com may earn a small commission at no extra cost to you.

This article was reviewed under TechLifeFuture’s citation-verification and EEAT-aligned process. Portions were AI-assisted and human-edited for accuracy and compliance.

© 2026 TechLifeFuture.com | Creative Commons BY-NC 4.0.