If your organization uses AI to advise clients—in finance, healthcare, law, or any professional service—you face a liability question that courts are answering right now: Who is responsible when the AI gets it wrong?The answer is clear and consistent across jurisdictions: You are. Not the AI vendor. Not the algorithm. The organization deploying the AI—and the professionals using it—remain fully liable for outputs that affect clients.

This article provides directors, licensed professionals, and platform operators with:

- Legal precedents: Court rulings from 2024-2025 establishing AI liability standards.

- Regulatory requirements: What FINRA, EU AI Act, and NIST now mandate

- Governance framework: The “Trust Layer” architecture organizations need.

Action checklist: What to implement in the next 90 days

The core message: AI amplifies both capability and liability. Organizations that document human oversight through frameworks like Verifiable Human Contribution (VHC) will prove compliance when regulators and insurers demand evidence. Those that cannot face uninsurable risk.

Reading time: 12 minutes

Target audience: Directors, C-suite executives, licensed professionals (financial advisors, lawyers, healthcare providers), platform operators

I. The Rise of AI as a “Co-Advisor” in Professional Practice

AI is Already Making Consequential Decisions

Financial advisors use robo-platforms to generate portfolio recommendations. Lawyers draft contracts with large language models. Doctors consult diagnostic AI for treatment plans. Mortgage brokers rely on algorithmic credit assessments.

These tools deliver real benefits:

- Speed: Analysis that took hours now takes seconds

- Precision: Pattern recognition humans cannot match

- Scale: Serving more clients with the same staff

- Cost reduction: Automating routine analytical work.

The Hidden Risk Multiplier

But AI also multiplies something less visible: liability exposure.

When a human advisor makes a mistake, the error is bounded to that one case. When an AI system generates thousands of recommendations daily, a systematic flaw can create mass exposure before anyone notices. A biased lending algorithm does not discriminate once—it discriminates at scale.

The liability paradox: The same speed and scale that make AI valuable make AI mistakes catastrophic.

II. The Legal Foundation: Why AI Does Not Remove Human Responsibility

Courts’ Emerging Consensus: “You Own What Your AI Says”

Three fundamental legal principles govern AI liability:

1. AI Has No Legal Personhood

Corporations can be sued. Humans can be sued. AI systems cannot. When an AI makes a mistake, liability flows upward to the humans and organizations that deployed it.

2. Professional Duties Are Technology-Neutral

Negligence, malpractice, and fiduciary duty existed before AI and continue unchanged after AI. Using AI to fulfill a professional obligation does not reduce the standard of care—if anything, courts suggest it may increase it by demanding oversight of the technology itself.

3. The “Reasonable Professional” Standard Evolves

Courts assess negligence by asking: “What would a reasonably careful professional do in these circumstances?” As AI adoption becomes standard practice, “reasonable care” increasingly includes understanding AI limitations, testing outputs, and maintaining human oversight.

Key insight: You cannot outsource accountability to an algorithm.

III. Landmark Cases: What Courts Have Already Decided

Case 1: Air Canada Chatbot Liability (2024)

Facts: Air Canada’s website chatbot provided incorrect information about bereavement fare policies. A customer relied on the chatbot’s advice, purchased a full-fare ticket, then sought the bereavement discount the chatbot had promised.

Air Canada’s defense: “The chatbot is a separate legal entity responsible for its own actions.”

Tribunal ruling: Rejected. Air Canada is liable for all information provided through its customer service channels, regardless of whether a human or AI generated the response.

Key quote: “While a chatbot has an interactive component, it is still just a part of Air Canada’s website. It should be obvious to Air Canada that it is responsible for all the information on its website.”

Source: American Bar Association Legal Technology Resource Center

Implications: Organizations cannot disclaim responsibility for AI outputs customers reasonably believe represent the company’s position.

Damages awarded: $650.88 CAD (fare difference) plus pre-judgment interest and tribunal fees. While financially trivial, the precedent is profound establishing that organizations cannot use the ‘technological veil’ defense to escape responsibility for AI outputs presented as authoritative company information.

Case 2: Workday Hiring Algorithm Discrimination (2024)

Facts: Class action lawsuit alleges Workday’s AI screening tools systematically discriminate against applicants over forty and those with disabilities, violating the Americans with Disabilities Act and Age Discrimination in Employment Act.

Significance: This case targets the AI vendor directly, not just the deploying employers, arguing the tool itself is the discriminatory instrument.

Current status: Federal court allowed portions of the case to proceed, rejecting Workday’s motion to dismiss.

Regulatory significance: The Equal Employment Opportunity Commission (EEOC) filed an amicus brief supporting the plaintiff’s position that AI vendors exercising control over hiring decisions can be directly liable as covered entities under anti-discrimination laws—a significant escalation of regulatory scrutiny beyond traditional employer-employee relationships.

Source: Reuters Legal Coverage

Implications:

- AI vendors face direct liability risk if their tools produce discriminatory outcomes.

- Deploying organizations face joint liability with vendors.

- “Black box” algorithms that cannot explain decisions face heightened scrutiny.

Case 3: Healthcare Algorithm Coverage Denials (2024-2025)

Facts: Multiple lawsuits allege health insurers use AI algorithms to deny medically necessary care at rates far exceeding human reviewer denial rates.

Key allegation: AI systems prioritize cost reduction over patient welfare, with inadequate human oversight to catch erroneous denials.

Legal theory: While insurers claim AI assists human decisions, evidence suggests humans “rubber stamp” algorithmic outputs without meaningful review—violating the duty to provide medical necessity determinations.

Implications for all sectors: Courts scrutinize whether human oversight is effective or merely nominal. The existence of a human “in the loop” is insufficient if that human cannot meaningfully override the AI.

Legal status (February 2025): The U.S. District Court for the District of Minnesota has allowed claims for breach of contract and breach of the implied covenant of good faith to proceed, rejecting UnitedHealthcare’s argument that the Medicare Act preempts state-law claims.

The Pattern Across Cases

Courts consistently reject three defense strategies:

❌ “The AI did it” → Liability flows to the deploying organization

❌ “The user accepted the terms.” → Terms cannot eliminate professional duties

❌ “A human was in the loop” → Must prove the human actually exercised judgment

✅ What courts accept: Evidence that qualified humans actively reviewed AI outputs, understood the reasoning, and made independent decisions documented in real time.

IV. Who Bears the Liability? Three Circles of Accountability

Visualization: The AI Accountability Stack

┌─────────────────────────────────────────┐

│ Licensed Professional (Front Line) │ ← Duty of care unchanged

│ • Lawyer, Doctor, Financial Advisor │ ← Must supervise AI outputs

│ • Cannot delegate judgment to AI │ ← Personal liability

└──────────────────┬──────────────────────┘

┌──────────────────▼──────────────────────┐

│ Deploying Organization (Platform) │ ← Strongest liability link

│ • Controls deployment decisions │ ← Owns client relationship

│ • Manages training and validation │ ← Vicarious liability for staff

└──────────────────┬──────────────────────┘

┌──────────────────▼──────────────────────┐

│ AI Developer (Vendor) │ ← Usually protected by contract

│ • Provides tools “as is” │ ← Product liability possible

│ • Disclaims fitness for purpose │ ← But increasingly challenged

└─────────────────────────────────────────┘

How Liability Typically Flows

Scenario: AI-powered financial advisor recommends an unsuitable investment. The client loses money.

Client sues the advisory firm (deploying organization) → ✅ Almost always successful.

Firm sues the licensed advisor (indemnification/contribution) → ✅ Likely if advisor ignored AI limitations.

Firm sues the AI vendor → ⚠️ Usually blocked by contract disclaimers unless it is gross negligence or fraud.

Key takeaway: The middle layer (deploying organization) bears the practical risk. Insurance, governance, and documentation become critical.

V. Regulatory Expectations: “Old Rules, New Tools” Across Professions

Financial Services: FINRA Notice 24-09

The Financial Industry Regulatory Authority clarified on June 27, 2024, that AI does not change compliance obligations.

Key requirements:

- Firms must supervise GenAI outputs as if they were human-generated.

- AI-assisted research, recommendations, and communications remain subject to FINRA Rule 2111 (Suitability) and Regulation Best Interest

- Firms cannot rely on AI vendors’ testing; they must independently validate tools for their specific use cases.

Source: FINRA Regulatory Notice 24-09 (June 27, 2024)

Practical impact: If your robo-advisor generates unsuitable portfolios, “the algorithm did it” is not a defense under best interest standards.

Healthcare: The Malpractice Standard Applies

Courts apply the traditional negligence test: What would a reasonably careful clinician do with this AI tool?

Medical societies, including the American Medical Associatio,n have issued guidance:

- Physicians remain responsible for all diagnoses and treatment decisions.

- AI is a clinical decision support tool, not a decision-maker.

- Adequate oversight requires understanding AI’s training data, limitations, and failure modes.

Source: New England Journal of Medicine – Liability in the Era of AI

Practical impact: “The AI recommended it” does not satisfy the standard of care if a reasonable physician would have questioned the output.

Legal Profession: Ethics Rules on Supervision

State bar associations increasingly treat AI as equivalent to a nonlawyer assistant under professional conduct rules.

Key requirements:

- Lawyers must ensure AI outputs are accurate before filing (Model Rule 1.1 – Competence)

- Confidential client information entered into AI tools must be protected (Model Rule 1.6 – Confidentiality)

- Lawyers cannot allow AI to make legal judgments (Model Rule 5.3 – Supervision of Nonlawyers)

Source: ABA Model Rules of Professional Conduct Commentary on Technology

Practical impact: A lawyer who submits AI-hallucinated case citations (as occurred in multiple 2023 sanctions cases) violates competence and candor duties.

Board-Level Governance: Directors’ Duty of Care Extends to AI

Directors of corporations deploying AI face fiduciary duties that increasingly include AI oversight.

Australian Institute of Company Directors (AICD) guidance:

Directors must understand how AI affects business models and risk profile.

Boards should question management on AI governance, validation, and incident response.

Failure to oversee AI systems affecting stakeholders may breach duty of care.

Source: AICD – A Director’s Guide to AI Governance

Practical impact: “We didn’t know our AI was biased” is not a valid director’s defense when the board failed to implement oversight systems.

VI. The Three Converging Crises Demanding Immediate Action

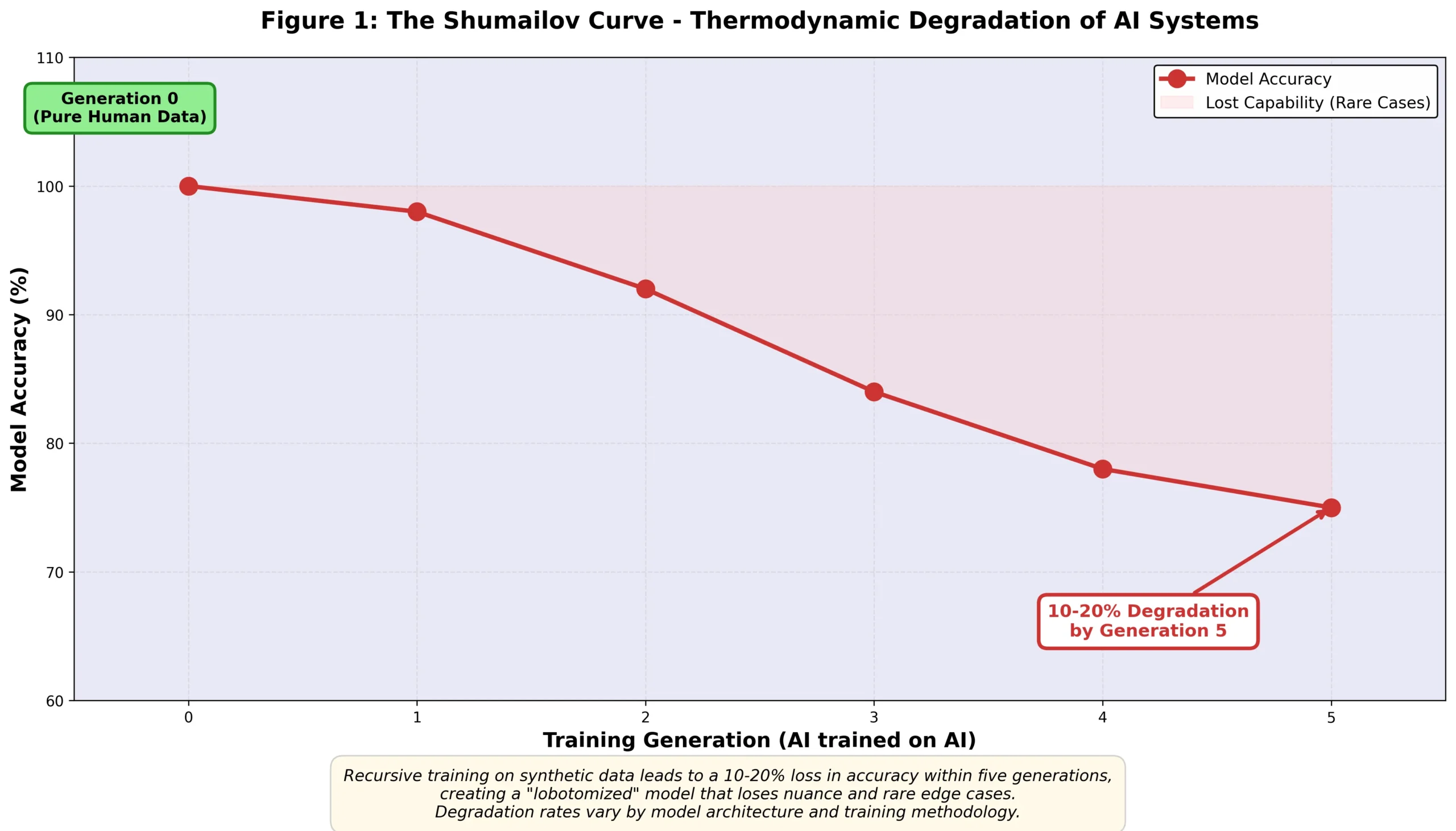

Crisis 1: Model Collapse (The Technical Crisis)

The threat: AI systems trained recursively on AI-generated data degrade in quality.

Research by Shumailov et al. (2023) demonstrates “model collapse”when generative AI is trained on outputs from previous AI generations, accuracy can drop 10-20% within five generations in specific experimental settings such as semantic accuracy tests with smaller models. The degradation rate varies by model architecture, training methodology, and data quality controls. The mechanism: AI models smooth out “tails” of probability distributions (rare, nuanced cases) in favor of common patterns, effectively “lobotomizing” the system.

Source: Shumailov et al., “The Curse of Recursion: Training on Generated Data Makes Models Forget” (2023)

Why directors care: Your AI vendor’s next model update might be worse than the current version if trained on degraded synthetic data. Organizations need provenance standards to filter training data.

The solution: Coalition for Content Provenance and Authenticity (C2PA) standards allow cryptographic tagging of human-generated vs. AI-generated content, protecting training data quality.

Crisis 2: Attribution Collapse (The Epistemic Crisis)

The threat: You cannot prove where AI’s information came from.

When an AI provides a recommendation, the user often cannot determine if the source is peer-reviewed research, a verified database, or a hallucination. This “attribution collapse” (a term describing the loss of epistemic provenance in AI systems) creates safety failures.

Research on multilingual AI safety shows models lose safety alignment when language context shifts—the system “forgets” that certain concepts are dangerous because the semantic link to its training is severed.

Source: Studies on attributional safety failures in code-mixed perturbations

Why directors care: If your AI gives bad advice, you cannot reconstruct the reasoning. In litigation, “we don’t know why the AI said that” is devastating.

The solution: Verifiable Human Contribution (VHC) frameworks log:

- What the AI suggested

- What the human reviewed, questioned, or changed

- Why was the final recommendation approved?

- Who made the decision and when?

This creates the audit trail that courts and regulators demand.

Crisis 3: Value Asymmetry (The Economic Crisis)

The threat: AI amplifies productivity but concentrates on wealth among platform owners, not contributors.

Research by Nobel laureate Daron Acemoglu shows AI may increase Total Factor Productivity by only 0.53-0.71% over ten years—far below industry hype—because current systems optimize for displacement (automating existing jobs) without reinstatement (creating new high-value jobs requiring human judgment).

Source: Acemoglu, “The Simple Macroeconomics of AI” NBER Working Paper 32487 (2024)

Geographic concentration: Projections indicate 70-75% of global AI value will be captured by just 10 nations by 2030, with the remaining 150+ countries sharing 25-30%.

Source: Digital Planet (Fletcher School), PwC Global AI Impact Analysis

Why directors care: If your organization relies on crowdsourced data, content moderators, or data labelers, you face ESG and reputational risk. Anthropologist Mary Gray’s research on “ghost work” documents millions performing invisible AI training labor without residual rights.

Source: Gray & Suri, “Ghost Work: How to Stop Silicon Valley from Building a New Global Underclass” (2019)

The solution: Fractional Attribution Innovation (FAIP) models use programmable IP (blockchain-based) to distribute value proportionally to verified contributors.

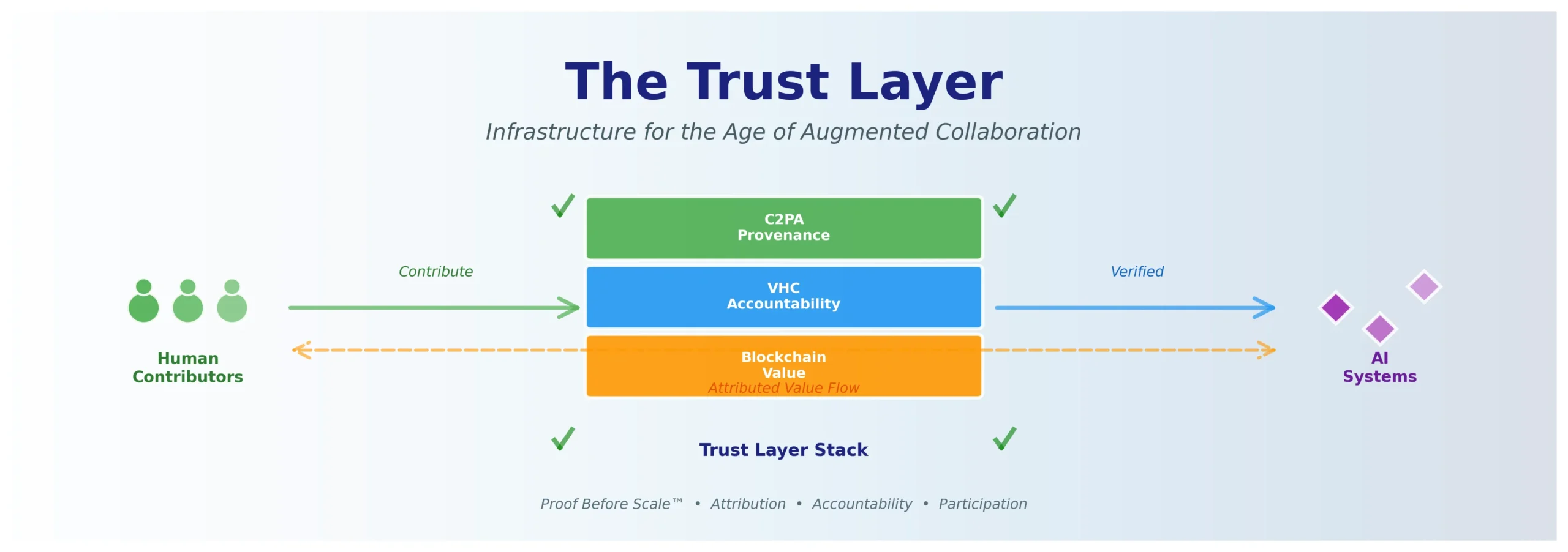

VII. The Trust Layer: Architecture for Sustainable AI

The Three-Layer Stack

Note: The following layers are numbered architecturally from foundation (Layer 1) to surface (Layer 3), while the diagram presents them visually from top to bottom for clarity.

Organizations demonstrating effective AI governance implement converging standards addressing each crisis:

╔════════════════════════════════════════════════════╗

║ LAYER 3: VALUE DISTRIBUTION ║

║ Programmable IP / Blockchain ║

║ → Solves: Value Asymmetry ║

║ → Standard: Story Protocol, Shapley Values ║

╠════════════════════════════════════════════════════╣

║ LAYER 2: PROCESS VERIFICATION ║

║ Verifiable Human Contribution (VHC) ║

║ → Solves: Attribution Collapse / Accountability ║

║ → Standard: ISO/IEC 42001, EU AI Act Article 14 ║

╠════════════════════════════════════════════════════╣

║ LAYER 1: CONTENT PROVENANCE ║

║ Coalition for Content Provenance (C2PA) ║

║ → Solves: Model Collapse / Truth Verification ║

║ → Standard: C2PA Technical Specification ║

╚════════════════════════════════════════════════════╝

Layer 1: C2PA (Provenance Layer)

Function: Cryptographically tags digital content with tamper-evident metadata showing origin, creation tool, and edit history.

Adoption: Operational today. Supported by Adobe, Microsoft, Intel. Camera manufacturers (Leica, Nikon) build “proof of humanity” at moment of capture.

Benefit for organizations: Protects training data quality by distinguishing human-generated (high-entropy) from AI-generated (low-entropy) content, preventing model collapse.

Source: C2PA Technical Specifications

Layer 2: VHC (Process Layer)

Function: Creates audit-ready evidence that qualified humans reviewed and documented AI-assisted outputs before consequential decisions.

Implementation: VHC systems log:

- Reviewer credentials (license number, competencies, training completion)

- Time spent on review (distinguishes “rubber stamp” from genuine oversight)

- Challenges raised (what the reviewer questioned or changed)

- Final decision rationale (why was the output approved or rejected)

Regulatory alignment:

- EU AI Act Article 14: Requires “effective” human oversight of high-risk AI systems, explicitly warning against automation bias.

- NIST AI Risk Management Framework: Emphasizes accountability and human-in-the-loop processes.

- ISO/IEC 42001: International standard for AI management systems (VHC provides evidence for human oversight controls)

Sources: EU AI Act Article 14 – Human Oversight, NIST AI Risk Management Framework

Practical example: A financial advisor uses a robo-platform to generate a retirement plan. VHC system logs:

Advisor spent 8 minutes reviewing the plan (not 30 seconds)

Questioned AI’s aggressive equity allocation for client age 62.

Adjusted allocation from 80/20 to 60/40 stocks/bonds.

Documented rationale: “Client has below-average risk tolerance based on stated goals; AI default allocation inappropriate for conservative investor profile.”

Result: If the client later claims unsuitable advice, the firm can prove the advisor actively exercised judgment rather than blindly accepting AI output.

Layer 3: Programmable IP (Value Layer)

- Function: Enables proportional, automated compensation for data and content contributors as AI systems generate value.

- Mechanism: Intellectual property registered on chain with embedded licensing terms (e.g., “0.001% royalty per model inference”). As AI agents access data, micropayments automatically execute via smart contracts.

- Mathematical framework: Uses Shapley Values from cooperative game theory to calculate each contributor’s marginal impact on model accuracy, enabling fair attribution in complex multi-contributor systems.

- Source: Story Protocol – Programmable IP Infrastructure

- Why organizations care: Transforms “ghost work” into verified, compensated contribution. Supports ESG compliance by demonstrating fair labor practices in AI supply chains.

VIII. Return on Intelligence (ROI²): The New Performance Metric

Beyond Traditional ROI

Traditional Return on Investment measures capital deployed and financial return. The AI era demands a new metric: Return on Intelligence (ROI²)—the combined efficacy of human insight multiplied by machine scale.

Formula: ROI² = Total Value Created / (Verified Human Contribution × AI Scale Factor)

Why most organizations cannot calculate ROI²: They cannot separate human contribution from AI amplification because they lack attribution systems.

The Trust Layer enables ROI² by:

- Logging human decision points (VHC)

- Tracking AI transformations (C2PA)

- Attributing downstream value (Programmable IP/FAIP)

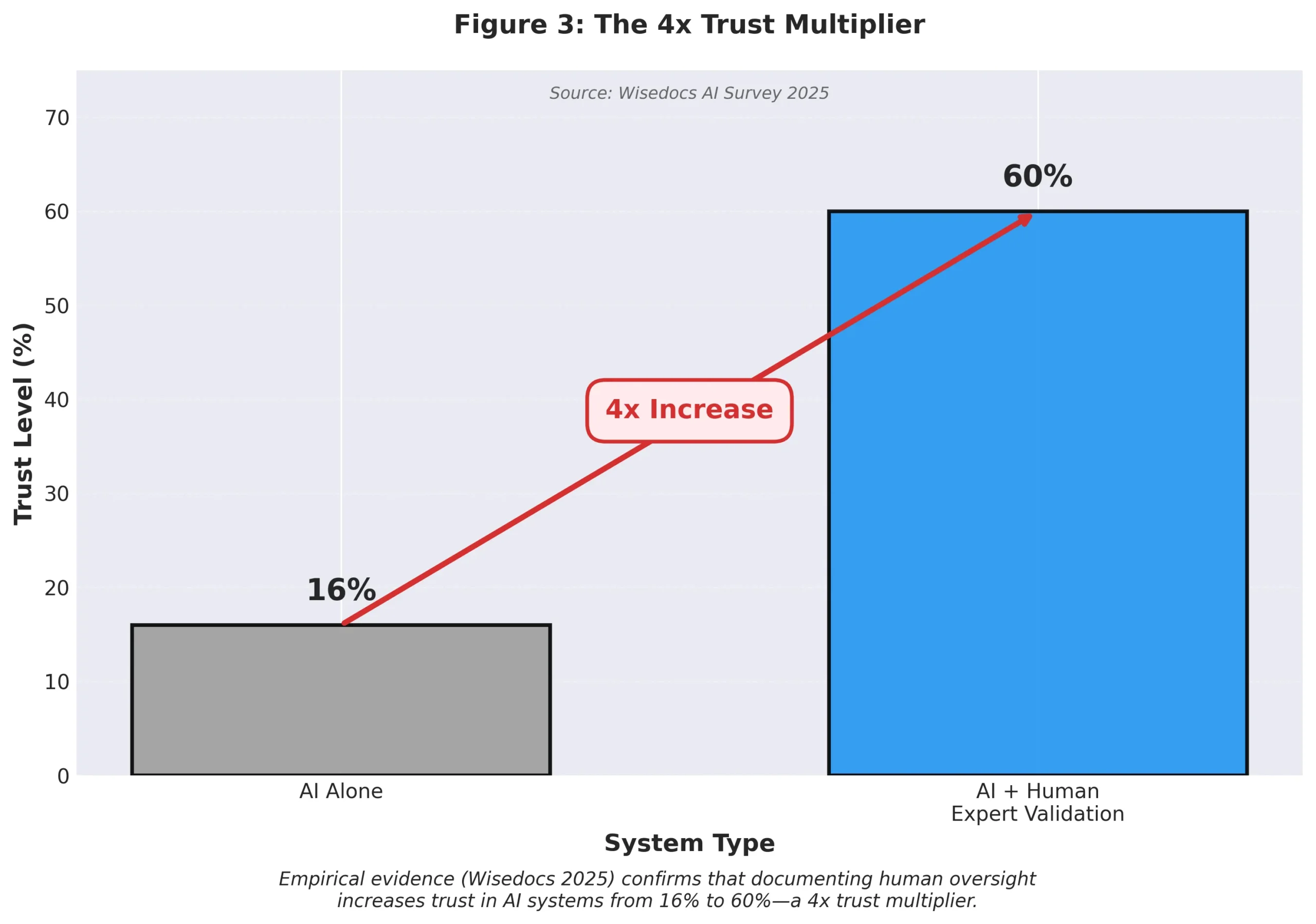

The 4x Trust Multiplier: Empirical Proof

Research on AI validation in insurance claims processing measured trust levels:

AI outputs alone: 16% high trust

AI + documented human expert validation: 60% high trust

Result: 4x increase in trust

Source: Wisedocs AI Survey 2024-2025

Commercial implications: Organizations implementing VHC can charge premium pricing for “Verified AI” services. In high-stakes sectors (healthcare, finance, legal), clients will pay more for documented human oversight.

Competitive advantage: When two advisory firms offer similar AI-powered services, the one that can prove human judgment was applied wins the trust-sensitive client.

IX. Practical Implementation: What to Do in the Next 90 Days

For Directors & Boards

Week 1-2: Discovery

[ ] Request AI inventory from management (what tools touch clients or material decisions?)

[ ] Review professional indemnity (PI), errors & omissions (E&O), and D&O insurance policies for AI coverage gaps.

[ ] Identify which AI deployments qualify as “high-risk” under emerging regulations.

Week 3-4: Governance Framework

[ ] Schedule board-level AI governance briefing with external expert.

[ ] Establish AI oversight committee or assign to existing risk/audit committee.

[ ] Define risk appetite for AI use in client-facing applications.

Week 5-8: Controls Implementation

[ ] Require management to implement human oversight checkpoints for client-facing AI.

[ ] Mandate VHC-style logging for high-stakes AI decisions

[ ] Establish incident reporting pathway for AI errors or near-misses.

Week 9-12: Monitoring & Reporting

[ ] Request quarterly reports on AI tool performance, overrides, and incidents.

[ ] Update board meeting agendas to include AI governance standing item.

[ ] Document board-level AI oversight in annual reporting (ESG/sustainability disclosures)

For Licensed Professionals (Advisors, Lawyers, Healthcare Providers)

Immediate Actions:

[ ] Create inventory of every AI tool used in client work (ChatGPT, robo-advisors, diagnostic AI, contract generators)

[ ] Document training received on each tool’s limitations and appropriate use.

[ ] Implement mandatory review checklist before finalizing AI-assisted work.

[ ] Update client engagement letters to disclose AI use and confirm human oversight.

[ ] Check professional liability insurance covers AI-assisted work (get written confirmation)

Documentation Standards: Every AI-assisted client deliverable should include:

What AI tool was used and for what purpose?

What the AI initially suggested (before human edits)

What the professional changed or overrode and why

Final sign-off with professional’s license number and date

Red flags requiring human escalation:

AI suggests action contrary to regulatory guidance.

AI output cannot be verified against source documents.

AI “hallucinates” facts, citations, or data.

AI recommendation seems plausible but feels “off.”

Remember: AI is a junior colleague, not a senior advisor. You own every output.

For Platform Operators & Technology Leaders

Technical Implementation:

[ ] Deploy C2PA content credentials for user-generated content and AI outputs.

[ ] Implement VHC logging middleware capture:

User ID, timestamp, AI model version

Input prompts and output generated.

Human review actions (edits, approvals, rejections)

Time spent in review (distinguish quick approval from thorough review)

[ ] Create API endpoints for regulatory/insurer audit access.

Governance Framework:

[ ] Establish Model Risk Management Committee

[ ] Document AI validation procedures (how you test for bias, accuracy, safety)

[ ] Create runbook for AI incident response.

[ ] Define criteria for model retirement (when to stop using a degraded system)

Insurance & Legal:

[ ] Engage insurers to transition from “silent AI” exposure to affirmative AI coverage.

[ ] Review vendor contracts for liability allocation and indemnification

[ ] Consider parametric insurance for AI-specific risks (hallucination events, mass errors)

The Regulatory Pincer Movement: Why You Have 18 Months

EU AI Act Phased Enforcement

Timeline for compliance:

August 2024: Prohibited AI practices (e.g., social scoring) banned.

August 2026: High-risk AI system requirements enforceable

August 2027: General-purpose AI model obligations apply.

Article 14 requirements for high-risk systems:

Systems must enable “effective” human oversight.

Humans must be able to “decide not to use… override or reverse the output.”

For biometric identification: minimum two human verifiers required.

Penalties: Up to €35 million or 7% of global turnover (for prohibited AI); €15 million or 3% of global turnover (for high-risk violations)

Source: EU AI Act Official Text – Regulation (EU) 2024/1689

NIST AI Risk Management Framework (US)

Status: Voluntary framework becoming de facto standard for courts and insurers assessing negligence.

Core requirements:

Governance structures for AI accountability

Risk identification and mitigation.

Transparency and explainability appropriate to context

Safety testing and monitoring

Impact on liability: Courts increasingly reference NIST framework when determining whether an organization exercised “reasonable care” in AI deployment.

Source: NIST AI Risk Management Framework

Copyright Office: Human Authorship Requirement

Guidance: US Copyright Office clarifies that AI-generated works not eligible for copyright unless sufficient human authorship is demonstrated.

IP trap: Organizations using AI to generate valuable content (software code, marketing copy, training materials) may lose IP protection if they cannot prove human “selection and arrangement.”

Solution: C2PA provenance + VHC documentation proves human creative contribution, preserving copyright eligibility.

Source: US Copyright Office – Copyright Registration Guidance: Works Containing Material Generated by Artificial Intelligence

The Strategic Choice: Verified Economy vs. Synthetic Entropy

Organizations face a binary future:

Path A: The Verified Economy (Trust Layer Implemented)

Characteristics:

Can prove human oversight when regulators audit.

Demonstrable compliance with EU AI Act, FINRA, professional standards

Insurable AI risk with favorable underwriting terms

Premium pricing for “Verified AI” services.

Protected training data (C2PA filtering prevents model collapse)

Sustainable contributor relationships (FAIP creates incentive alignment)

Competitive advantages:

Win trust-sensitive clients (healthcare systems, regulated financial institutions, government agencies)

Attract and retain top professional talent (who will not risk license on unverifiable AI)

Command premium pricing (4x trust multiplier justifies higher fees)

Defensible in litigation (contemporaneous evidence of human judgment)

Path B: Synthetic Entropy (Trust Layer Absent)

Characteristics:

Cannot prove human oversight (“the AI did it” is only defense)

Regulatory exposure (Article 14 violations, professional conduct breaches)

Uninsurable risk (PI/E&O carriers exclude or price at penalty rates)

Commodity pricing pressure (competing on “cheap AI automation”)

Degrading model quality (training data polluted with synthetic outputs)

Contributor exodus (top talent migrates to verified platforms)

Existential risks:

Lose major clients requiring verifiable governance.

Professional license sanctions for unverifiable AI-assisted work

Uninsurable following first major claim

Trapped in race-to-bottom pricing.

Model collapse makes AI tools unreliable.

The 18-Month Window

Why urgency matters:

Regulatory enforcement begins: EU AI Act high-risk requirements enforceable August 2026 (18 months from now)

Insurance markets repricing: Underwriters demanding VHC-style evidence for 2026 renewals.

Competitive separation: Early adopters establishing “Verified AI” market position.

Talent flight: Best professionals refusing to work without documentation safeguards.

Data degradation: Public training data quality declines as synthetic content proliferates.

Organizations implementing Trust Layer architecture in 2025 will dominate 2026-2027. Those waiting will face crisis implementation at a higher cost.

Frequently Asked Questions (FAQs)

Q: Who is liable when AI gives bad advice?

Answer: The organization deploying the AI—not the AI itself, and usually not just the vendor—remains responsible for advice affecting clients.

The Air Canada chatbot tribunal explicitly rejected the argument that AI is a “separate legal entity.” Courts hold that customers cannot distinguish between human and AI outputs, so organizations bear liability for both.

Source: American Bar Association – Air Canada Chatbot Case Analysis

Q: Can a company argue “the chatbot did it” as a legal defense?

Answer: No. Courts consistently reject this defense across jurisdictions. The legal principle: Organizations are responsible for all outputs from their systems, regardless of whether a human or algorithm generated the content. Using AI does not create a liability shield.

Source: The Guardian – Air Canada Chatbot Lawsuit Coverage

Q: Can AI vendors be sued directly, or only the organizations using their tools?

Answer: Both can be sued, though vendor liability is more complex.

The Workday hiring bias litigation demonstrates that vendors face direct liability exposure if their AI tools produce discriminatory outcomes. However, most vendor contracts include extensive liability limitations, making the deploying organization the more practical defendant.

Strategy: Organizations should negotiate for vendor indemnification and require evidence vendors evaluated for bias, accuracy, and safety.

Source: Reuters – Workday Must Face Bias Claims Over AI

Q: Does using AI change professional malpractice rules for doctors, lawyers, or financial advisors?

Answer: No. Professional standards and duties of care remain unchanged.

Regulators and courts apply a “technology-neutral” approach: the duty to provide competent, suitable advice persists regardless of tools used. If anything, AI may increase the standard of care by requiring professionals to understand and supervise the technology.

Financial services: FINRA Notice 24-09 clarifies that suitability and best interest duties apply identically to AI-assisted advice

Healthcare: Traditional negligence test applies (what would a careful physician do with this AI tool?)

Legal: AI is treated as a non-lawyer assistant requiring attorney supervision.

Sources: FINRA Regulatory Notice 24-09, New England Journal of Medicine – AI Liability Article, ABA Model Rules – Technology Commentary

Q: Does professional indemnity (PI) insurance cover AI-related mistakes?

Answer: Usually yes—if you can demonstrate effective human oversight.

Current PI policies typically cover AI-assisted work as an extension of normal professional services. However, insurers are increasingly asking:

What AI tools do you use and for what purposes?

What controls and sign-offs exist?

Can you reconstruct decisions if there is a claim?

Organizations implementing VHC-style documentation can answer these questions confidently. Those who cannot face coverage disputes or policy exclusions.

Trend: Insurers moving from “silent AI” (unintended coverage) to “affirmative AI” policies with explicit terms—but only for organizations demonstrating governance.

Source: Informed Professional – Professional Indemnity and AI Liability

Q: What is “silent AI” and why is it risky?

Answer: “Silent AI” describes AI usage not explicitly recognized in policies, contracts, or controls—creating unpriced, unmanaged liability exposure.

The term emerged in insurance markets (similar to earlier “silent cyber” debates). When organizations deploy AI without disclosing use to insurers or implementing governance, they create:

Mispriced risk: Insurers cannot properly underwrite what they do not know about

Coverage disputes: “Your policy doesn’t cover AI losses” arguments in claims.

Regulatory exposure: Cannot prove compliance if AI use is not documented.

Solution: Make AI use explicit through:

Disclosure to insurers

Documented governance frameworks

VHC-style audit trails

Source: Insurance industry commentary on silent AI exposure (parallel to silent cyber evolution)

Q: Is there an AI liability gap where no one is clearly responsible?

Answer: Partially yes, especially for “black box” AI systems where decision-making is opaque.

- European Commission analysis identifies gaps in existing liability frameworks, particularly for:

- AI systems where no single party controls outcomes

- Cascading failures across interconnected AI systems

- Damage occurred far downstream from the initial AI decision.

However, courts are increasingly holding deploying organizations responsible regardless of AI complexity—the liability gap is closing through case law.

Source: Eversheds Sutherland – Product Liability for AI Systems (EU Analysis)

Q: What are the specific risks of using AI hiring and screening tools?

Answer: Algorithmic bias, discrimination claims, and regulatory penalties. Documented risks include:

- Age discrimination: AI screening tools allegedly filtering out workers 40+ (Workday litigation)

- Disability discrimination: Video interview AI penalizing speech patterns associated with disabilities.

- Racial bias: Facial recognition and voice analysis tools are performing poorly on non-white candidates.

- Legal exposure: Both vendors and deploying employers face liability under ADA, ADEA, Title VII, and state civil rights laws.

- Mitigation: Require bias audits from vendors, implement human review of all AI-flagged rejections, and document testing for disparate impact.

Source: ClassAction.org – AI Interview & Screening Tool Lawsuits

Q: How can firms reduce AI liability exposure?

Answer: Implement the five-pillar governance framework:

- Policy & Process: Formal AI use policy approved by the board. Approval of gates for new AI tools, clear ownership and accountability

- Model Governance: Validation and accuracy testing before deployment, Ongoing performance monitoring, Bias audits at regular intervals Incident logging and escalation pathways

- Human Oversight (VHC): Mandatory review checkpoints for high-stakes outputs. Time-stamped documentation of review. Evidence of challenges and overrides. Sign-off by qualified professionals.

- Training & Competence: Continuous education on AI limitations. Documented learning pathways. Competency assessments

- Insurance Strategy: Disclose AI to insurers proactively. Seek affirmative AI coverage terms. Negotiate vendor indemnification. Maintaining evidence governance prevents claims.

Source: Mayer Brown – FINRA Regulatory Notice 24-09 Analysis

Q: Should AI governance be a board-level risk category?

Answer: Yes. AI affects strategic, financial, operational, and reputational risk—all board responsibilities. Directors’ fiduciary duties now include:

- Understanding how AI affects business models.

- Overseeing AI governance implementation

- Questioning management on validation, testing, and monitoring

- Ensuring culture does not encourage over-reliance on AI.

- Protecting against regulatory and liability exposure

Boards that treat AI as “just a technology issue” for IT departments will face questions in future disputes about whether they exercised adequate oversight.

Sources: Australian Institute of Company Directors – AI Governance Guide

Eversheds Sutherland – AI Product Liability EU

Recommended Resources: Videos

Stanford HAI — Understanding Liability Risk from Using Healthcare AI Tools

Why watch: Stanford’s Human-Centered AI Institute analyzes how medical malpractice liability applies to clinical AI tools. Relevant beyond healthcare—governance principles translate to any professional advice context.

Key takeaway: Courts will assess whether the professional understood the AI’s limitations and exercised independent judgment, not merely whether they “used” the AI.

Stimson Center / Washington Foreign Law Society — AI, Liability & Risk in Generative AI

Why watch: Legal experts discuss emerging liability frameworks for generative AI across sectors. Covers product liability, professional liability, and regulatory approaches.

Key takeaway: The “AI did it” defense fails because legal systems require human accountability for consequential decisions.

Conclusion: The Choice Facing Organizations in 2025

AI will deeply shape professional advice, operational decisions, and client relationships. Human accountability is not going away—if anything is intensifying.

Winners in the AI-augmented economy will be organizations that:

- Adopt responsibly: Implement governance before regulators mandate it.

- Document transparently: Create audit trails proving human judgment.

- Price for trust: Charge premium for verified AI vs. commodity automation.

- Sustain quality: Protect training data and contributor relationships.

The Trust Layer—C2PA provenance, VHC process verification, and programmable IP value distribution—provides the architecture for this transition. Organizations have approximately 18 months before regulatory enforcement, insurance repricing, and market separation make late adoption prohibitively expensive. The question is not whether to implement AI governance, but whether you will architect for verified sustainability or optimize for synthetic extraction. The Age of Augmented Collaboration rewards those who scale with verification, not velocity alone.

Mandatory Disclosure Block

This article reflects AI, regulatory, insurance, and professional services practices as of 10 January 2026 (AEST). Readers should confirm whether subsequent guidance has been issued by their regulators, professional bodies, insurers, or standard-setting organizations.

Content on TechLifeFuture.com is for educational and informational purposes only and does not constitute legal, accounting, financial, credit, or insurance advice. It is not a substitute for tailored professional advice in your jurisdiction.

Some links on this page may be affiliate or referral links (including, where relevant, Educative.io, Mindhive.ai, or other partners). If you purchase through these links, TechLifeFuture.com may earn a small commission at no extra cost to you.

Conflict-of-interest and IP disclosure: The author, John Richard Cosstick, is the named inventor on the following pending patent applications related to concepts discussed in this article:

- Verifiable Human Contribution (VHC): Australian patent application pending 2025220863, international application number PCT/IB2025/058808

- AI Management Systems (AIMS): Australian patent application pending 2025271387, international application number PCT/AU2025/051428

These applications formed the conceptual framing of Verifiable Human Contribution (VHC) and AI Management Systems (AIMS) discussed in this article.

This article was reviewed under TechLifeFuture’s citation-verification and EEAT-aligned editorial process. Portions were AI-assisted and human-edited for accuracy, clarity, and compliance with professional publishing standards.

© 2026 TechLifeFuture.com | Creative Commons BY-NC 4.0